We Think Thirumalai Chemicals (NSE:TIRUMALCHM) Has A Fair Chunk Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Thirumalai Chemicals Limited (NSE:TIRUMALCHM) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Thirumalai Chemicals

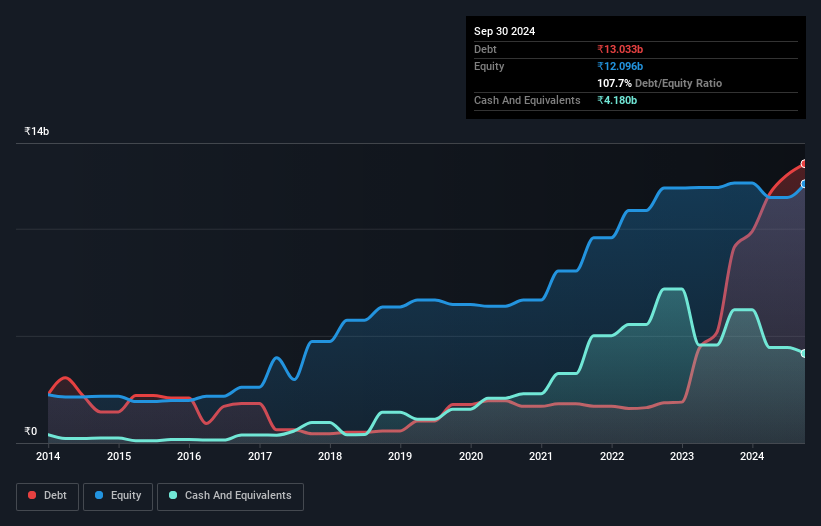

What Is Thirumalai Chemicals's Debt?

As you can see below, at the end of September 2024, Thirumalai Chemicals had ₹13.0b of debt, up from ₹9.15b a year ago. Click the image for more detail. However, it does have ₹4.18b in cash offsetting this, leading to net debt of about ₹8.85b.

How Strong Is Thirumalai Chemicals' Balance Sheet?

The latest balance sheet data shows that Thirumalai Chemicals had liabilities of ₹9.73b due within a year, and liabilities of ₹12.9b falling due after that. On the other hand, it had cash of ₹4.18b and ₹2.10b worth of receivables due within a year. So its liabilities total ₹16.3b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Thirumalai Chemicals is worth ₹33.0b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. When analysing debt levels, the balance sheet is the obvious place to start. But it is Thirumalai Chemicals's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Thirumalai Chemicals reported revenue of ₹21b, which is a gain of 4.7%, although it did not report any earnings before interest and tax. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Thirumalai Chemicals had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at ₹7.2m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through ₹5.0b of cash over the last year. So in short it's a really risky stock. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with Thirumalai Chemicals , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Thirumalai Chemicals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TIRUMALCHM

Thirumalai Chemicals

Manufactures and sells organic chemicals in India and internationally.

Low and slightly overvalued.

Similar Companies

Market Insights

Community Narratives