Is Sumitomo Chemical India (NSE:SUMICHEM) A Compounding Machine?

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, the ROCE of Sumitomo Chemical India (NSE:SUMICHEM) looks attractive right now, so lets see what the trend of returns can tell us.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Sumitomo Chemical India:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

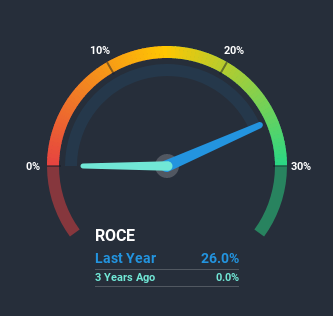

0.26 = ₹3.9b ÷ (₹26b - ₹12b) (Based on the trailing twelve months to September 2020).

So, Sumitomo Chemical India has an ROCE of 26%. In absolute terms that's a great return and it's even better than the Chemicals industry average of 14%.

Check out our latest analysis for Sumitomo Chemical India

In the above chart we have measured Sumitomo Chemical India's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

The Trend Of ROCE

Sumitomo Chemical India deserves to be commended in regards to it's returns. Over the past two years, ROCE has remained relatively flat at around 26% and the business has deployed 44% more capital into its operations. Returns like this are the envy of most businesses and given it has repeatedly reinvested at these rates, that's even better. You'll see this when looking at well operated businesses or favorable business models.

On a side note, Sumitomo Chemical India's current liabilities are still rather high at 44% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.The Key Takeaway

In the end, the company has proven it can reinvest it's capital at high rates of returns, which you'll remember is a trait of a multi-bagger. Therefore it's no surprise that shareholders have earned a respectable 54% return if they held over the last year. So even though the stock might be more "expensive" than it was before, we think the strong fundamentals warrant this stock for further research.

Before jumping to any conclusions though, we need to know what value we're getting for the current share price. That's where you can check out our FREE intrinsic value estimation that compares the share price and estimated value.

High returns are a key ingredient to strong performance, so check out our free list ofstocks earning high returns on equity with solid balance sheets.

If you decide to trade Sumitomo Chemical India, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:SUMICHEM

Sumitomo Chemical India

Engages in the manufacture and sale of household and public health insecticides, agricultural pesticides, and animal nutrition products in India and internationally.

Flawless balance sheet with solid track record.