- India

- /

- Metals and Mining

- /

- NSEI:SHAHALLOYS

We Think Shah Alloys (NSE:SHAHALLOYS) Is Taking Some Risk With Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Shah Alloys Limited (NSE:SHAHALLOYS) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Shah Alloys

What Is Shah Alloys's Net Debt?

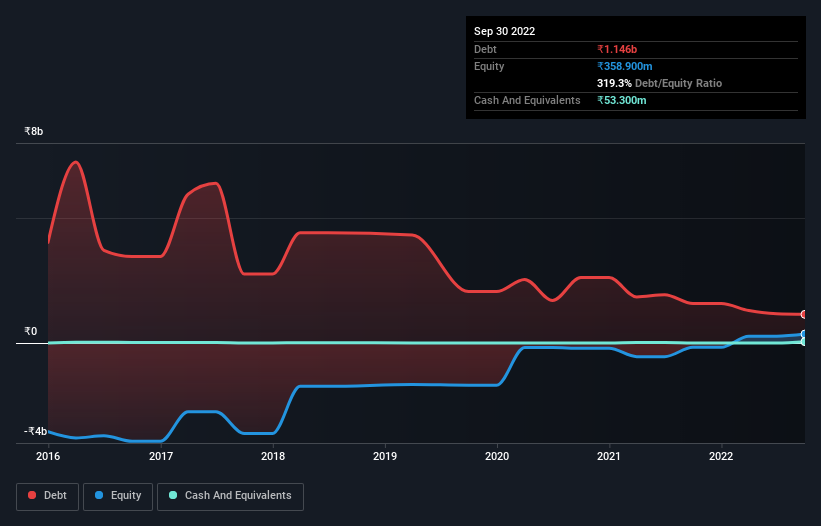

You can click the graphic below for the historical numbers, but it shows that Shah Alloys had ₹1.15b of debt in September 2022, down from ₹1.58b, one year before. However, it also had ₹53.3m in cash, and so its net debt is ₹1.09b.

A Look At Shah Alloys' Liabilities

According to the last reported balance sheet, Shah Alloys had liabilities of ₹2.22b due within 12 months, and liabilities of ₹284.0m due beyond 12 months. Offsetting this, it had ₹53.3m in cash and ₹52.4m in receivables that were due within 12 months. So its liabilities total ₹2.40b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the ₹1.34b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Shah Alloys would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Shah Alloys has a low net debt to EBITDA ratio of only 1.5. And its EBIT covers its interest expense a whopping 30.5 times over. So we're pretty relaxed about its super-conservative use of debt. In fact Shah Alloys's saving grace is its low debt levels, because its EBIT has tanked 21% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Shah Alloys will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last two years, Shah Alloys generated free cash flow amounting to a very robust 88% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Our View

To be frank both Shah Alloys's EBIT growth rate and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But on the bright side, its interest cover is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that Shah Alloys's debt is making it a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 3 warning signs we've spotted with Shah Alloys (including 1 which is concerning) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SHAHALLOYS

Shah Alloys

Engages in the manufacture and sale of flat and long stainless steel, alloy and special steel, carbon/mild steel, and armor steel products in India and internationally.

Low and slightly overvalued.

Market Insights

Community Narratives