Advertisement

Privi Speciality Chemicals (NSE:PRIVISCL) Will Pay A Larger Dividend Than Last Year At ₹5.00

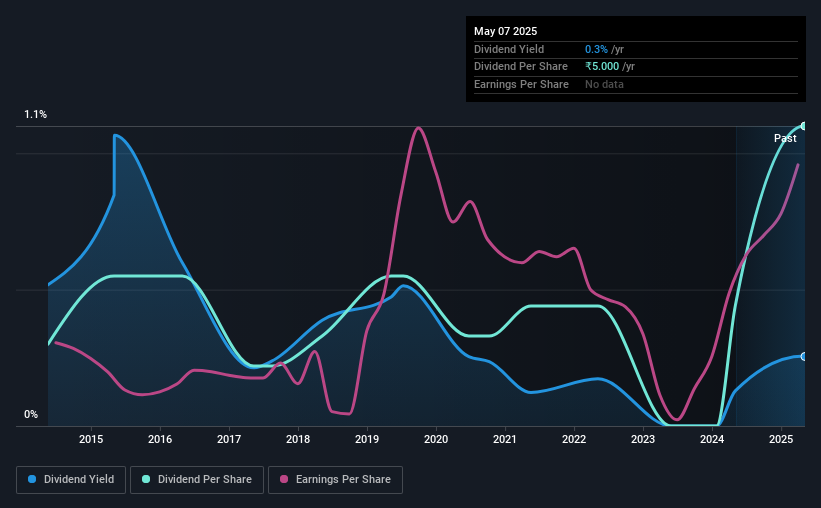

Privi Speciality Chemicals Limited (NSE:PRIVISCL) will increase its dividend from last year's comparable payment on the 31st of August to ₹5.00. Despite this raise, the dividend yield of 0.3% is only a modest boost to shareholder returns.

Our free stock report includes 2 warning signs investors should be aware of before investing in Privi Speciality Chemicals. Read for free now.Privi Speciality Chemicals' Payment Could Potentially Have Solid Earnings Coverage

Even a low dividend yield can be attractive if it is sustained for years on end. Based on the last payment, Privi Speciality Chemicals was earning enough to cover the dividend, but free cash flows weren't positive. We think that cash flows should take priority over earnings, so this is definitely a worry for the dividend going forward.

If the trend of the last few years continues, EPS will grow by 5.1% over the next 12 months. Assuming the dividend continues along recent trends, we think the payout ratio could be 11% by next year, which is in a pretty sustainable range.

See our latest analysis for Privi Speciality Chemicals

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. The dividend has gone from an annual total of ₹1.36 in 2015 to the most recent total annual payment of ₹5.00. This implies that the company grew its distributions at a yearly rate of about 14% over that duration. Privi Speciality Chemicals has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Has Growth Potential

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. We are encouraged to see that Privi Speciality Chemicals has grown earnings per share at 5.1% per year over the past five years. Privi Speciality Chemicals definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

Our Thoughts On Privi Speciality Chemicals' Dividend

Overall, we always like to see the dividend being raised, but we don't think Privi Speciality Chemicals will make a great income stock. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. We don't think Privi Speciality Chemicals is a great stock to add to your portfolio if income is your focus.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 2 warning signs for Privi Speciality Chemicals (of which 1 can't be ignored!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PRIVISCL

Privi Speciality Chemicals

Operates as a manufacturer, supplier, and exporter of aroma and fragrance chemicals in India, North America, Asia, the Middle East, Africa, Europe, South America, and the United Kingdom.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor