- India

- /

- Basic Materials

- /

- NSEI:MANGLMCEM

Would Shareholders Who Purchased Mangalam Cement's (NSE:MANGLMCEM) Stock Three Years Be Happy With The Share price Today?

Mangalam Cement Limited (NSE:MANGLMCEM) shareholders should be happy to see the share price up 14% in the last month. But that doesn't change the fact that the returns over the last three years have been less than pleasing. In fact, the share price is down 42% in the last three years, falling well short of the market return.

See our latest analysis for Mangalam Cement

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

During the unfortunate three years of share price decline, Mangalam Cement actually saw its earnings per share (EPS) improve by 31% per year. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Or else the company was over-hyped in the past, and so its growth has disappointed.

It's worth taking a look at other metrics, because the EPS growth doesn't seem to match with the falling share price.

With a rather small yield of just 0.5% we doubt that the stock's share price is based on its dividend. We note that, in three years, revenue has actually grown at a 8.0% annual rate, so that doesn't seem to be a reason to sell shares. This analysis is just perfunctory, but it might be worth researching Mangalam Cement more closely, as sometimes stocks fall unfairly. This could present an opportunity.

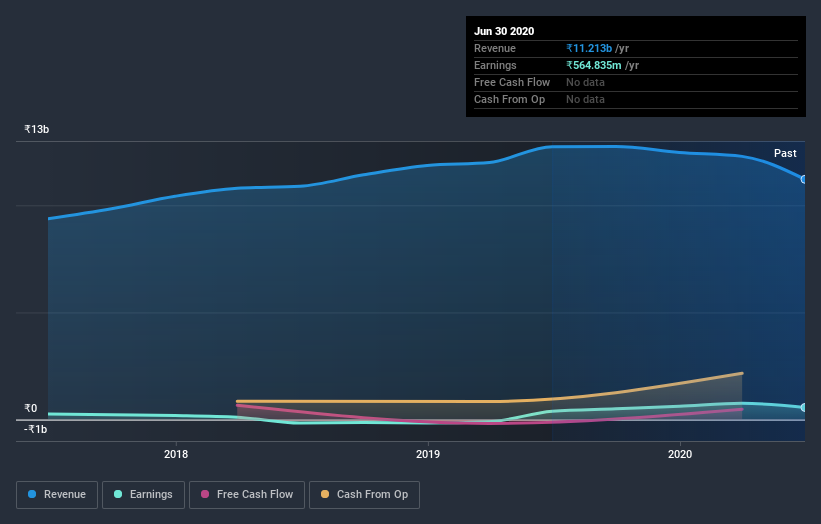

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

It's probably worth noting we've seen significant insider buying in the last quarter, which we consider a positive. On the other hand, we think the revenue and earnings trends are much more meaningful measures of the business. It might be well worthwhile taking a look at our free report on Mangalam Cement's earnings, revenue and cash flow.

A Different Perspective

Investors in Mangalam Cement had a tough year, with a total loss of 33% (including dividends), against a market gain of about 4.3%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Longer term investors wouldn't be so upset, since they would have made 1.0%, each year, over five years. If the fundamental data continues to indicate long term sustainable growth, the current sell-off could be an opportunity worth considering. It's always interesting to track share price performance over the longer term. But to understand Mangalam Cement better, we need to consider many other factors. Take risks, for example - Mangalam Cement has 2 warning signs (and 1 which shouldn't be ignored) we think you should know about.

Mangalam Cement is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on IN exchanges.

When trading Mangalam Cement or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:MANGLMCEM

Mangalam Cement

Manufactures and sells cement and clinker primarily in India.

Reasonable growth potential with acceptable track record.