Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:KIRLOSIND

Insiders of Kirloskar Industries Limited (NSE:KIRLOSIND) must be frustrated after market cap dropped ₹4.8b since recent purchases

Key Insights

- Insiders appear to have a vested interest in Kirloskar Industries' growth, as seen by their sizeable ownership

- The top 3 shareholders own 51% of the company

- Insiders have bought recently

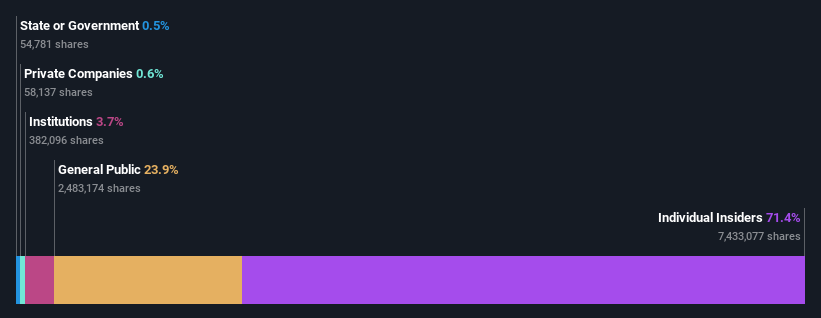

If you want to know who really controls Kirloskar Industries Limited (NSE:KIRLOSIND), then you'll have to look at the makeup of its share registry. The group holding the most number of shares in the company, around 71% to be precise, is individual insiders. That is, the group stands to benefit the most if the stock rises (or lose the most if there is a downturn).

And looking at our data, we can see that insiders have bought shares recently. However, with shares price down 11% last week, they must be disappointed.

In the chart below, we zoom in on the different ownership groups of Kirloskar Industries.

Check out our latest analysis for Kirloskar Industries

What Does The Institutional Ownership Tell Us About Kirloskar Industries?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

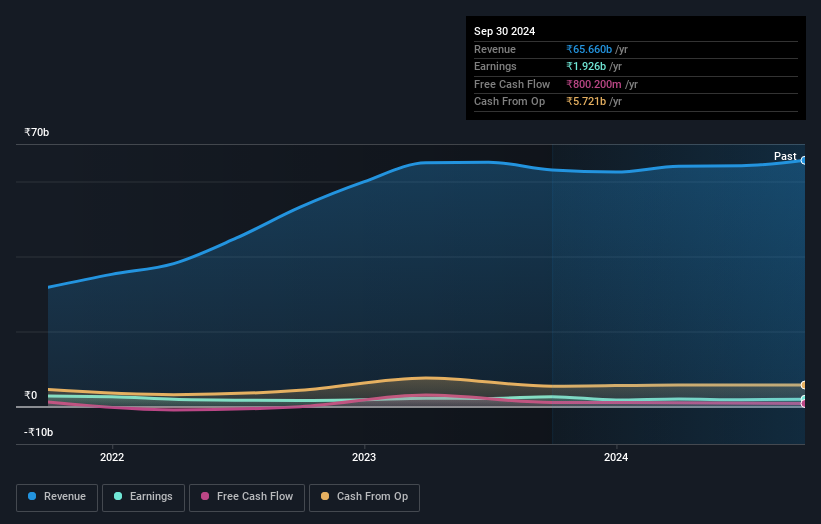

Institutions have a very small stake in Kirloskar Industries. That indicates that the company is on the radar of some funds, but it isn't particularly popular with professional investors at the moment. If the business gets stronger from here, we could see a situation where more institutions are keen to buy. We sometimes see a rising share price when a few big institutions want to buy a certain stock at the same time. The history of earnings and revenue, which you can see below, could be helpful in considering if more institutional investors will want the stock. Of course, there are plenty of other factors to consider, too.

We note that hedge funds don't have a meaningful investment in Kirloskar Industries. The company's largest shareholder is Rahul Kirloskar, with ownership of 22%. Meanwhile, the second and third largest shareholders, hold 17% and 11%, of the shares outstanding, respectively. Furthermore, CEO Mahesh Chhabria is the owner of 1.2% of the company's shares.

After doing some more digging, we found that the top 3 shareholders collectively control more than half of the company's shares, implying that they have considerable power to influence the company's decisions.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock's expected performance. As far as we can tell there isn't analyst coverage of the company, so it is probably flying under the radar.

Insider Ownership Of Kirloskar Industries

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

Insider ownership is positive when it signals leadership are thinking like the true owners of the company. However, high insider ownership can also give immense power to a small group within the company. This can be negative in some circumstances.

It seems that insiders own more than half the Kirloskar Industries Limited stock. This gives them a lot of power. That means they own ₹28b worth of shares in the ₹39b company. That's quite meaningful. Most would argue this is a positive, showing strong alignment with shareholders. You can click here to see if those insiders have been buying or selling.

General Public Ownership

The general public-- including retail investors -- own 24% stake in the company, and hence can't easily be ignored. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Kirloskar Industries , and understanding them should be part of your investment process.

Of course this may not be the best stock to buy. Therefore, you may wish to see our free collection of interesting prospects boasting favorable financials.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if Kirloskar Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KIRLOSIND

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor