- India

- /

- Metals and Mining

- /

- NSEI:JAIBALAJI

We Think Jai Balaji Industries' (NSE:JAIBALAJI) Profit Is Only A Baseline For What They Can Achieve

Even though Jai Balaji Industries Limited's (NSE:JAIBALAJI) recent earnings release was robust, the market didn't seem to notice. We think that investors have missed some encouraging factors underlying the profit figures.

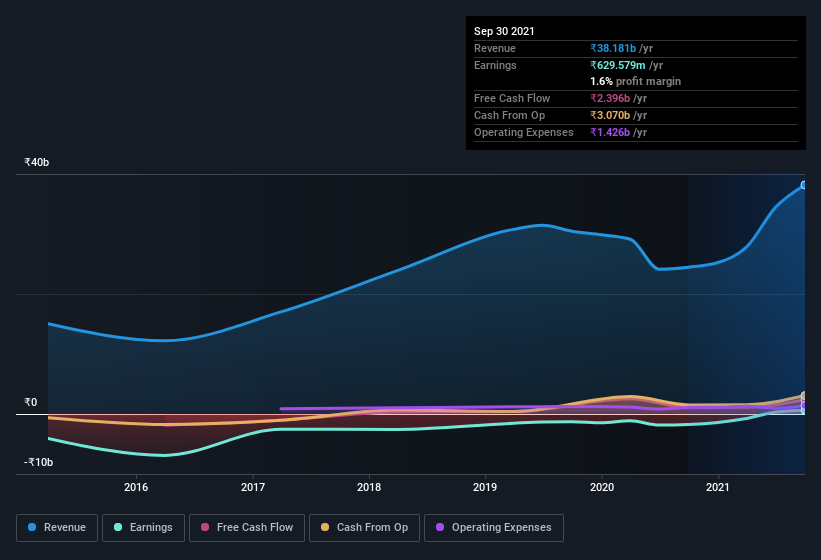

Check out our latest analysis for Jai Balaji Industries

Examining Cashflow Against Jai Balaji Industries' Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Jai Balaji Industries has an accrual ratio of -0.11 for the year to September 2021. That indicates that its free cash flow was a fair bit more than its statutory profit. In fact, it had free cash flow of ₹2.4b in the last year, which was a lot more than its statutory profit of ₹629.6m. Jai Balaji Industries shareholders are no doubt pleased that free cash flow improved over the last twelve months.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Jai Balaji Industries.

Our Take On Jai Balaji Industries' Profit Performance

As we discussed above, Jai Balaji Industries has perfectly satisfactory free cash flow relative to profit. Based on this observation, we consider it likely that Jai Balaji Industries' statutory profit actually understates its earnings potential! And it's also positive that the company showed enough improvement to book a profit this year, after losing money last year. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. To help with this, we've discovered 3 warning signs (2 are a bit concerning!) that you ought to be aware of before buying any shares in Jai Balaji Industries.

Today we've zoomed in on a single data point to better understand the nature of Jai Balaji Industries' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:JAIBALAJI

Jai Balaji Industries

Manufactures and markets iron and steel products primarily in India.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion