Advertisement

Hindprakash Industries Limited (NSE:HPIL) Is Going Strong But Fundamentals Appear To Be Mixed : Is There A Clear Direction For The Stock?

Most readers would already be aware that Hindprakash Industries' (NSE:HPIL) stock increased significantly by 36% over the past month. However, we wonder if the company's inconsistent financials would have any adverse impact on the current share price momentum. Particularly, we will be paying attention to Hindprakash Industries' ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for Hindprakash Industries

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Hindprakash Industries is:

6.6% = ₹24m ÷ ₹365m (Based on the trailing twelve months to March 2021).

The 'return' is the yearly profit. One way to conceptualize this is that for each ₹1 of shareholders' capital it has, the company made ₹0.07 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Hindprakash Industries' Earnings Growth And 6.6% ROE

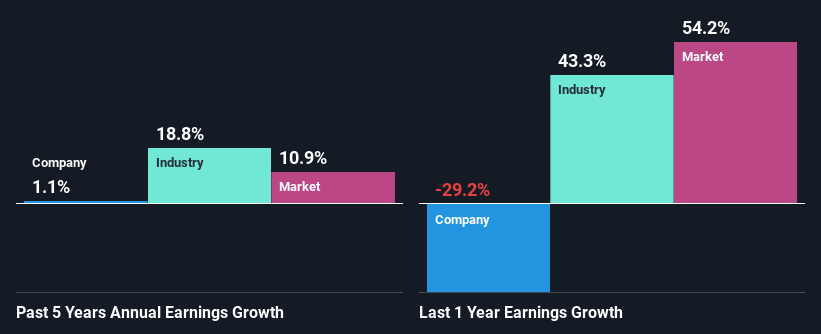

It is quite clear that Hindprakash Industries' ROE is rather low. Not just that, even compared to the industry average of 15%, the company's ROE is entirely unremarkable. Hence, the flat earnings seen by Hindprakash Industries over the past five years could probably be the result of it having a lower ROE.

Next, on comparing with the industry net income growth, we found that Hindprakash Industries' reported growth was lower than the industry growth of 19% in the same period, which is not something we like to see.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Hindprakash Industries''s valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Hindprakash Industries Efficiently Re-investing Its Profits?

Hindprakash Industries' low three-year median payout ratio of 24% (implying that the company keeps76% of its income) should mean that the company is retaining most of its earnings to fuel its growth and this should be reflected in its growth number, but that's not the case.

Additionally, Hindprakash Industries started paying a dividend only recently. So it looks like the management must have perceived that shareholders favor dividends over earnings growth.

Summary

Overall, we have mixed feelings about Hindprakash Industries. While the company does have a high rate of reinvestment, the low ROE means that all that reinvestment is not reaping any benefit to its investors, and moreover, its having a negative impact on the earnings growth. Up till now, we've only made a short study of the company's growth data. You can do your own research on Hindprakash Industries and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

Valuation is complex, but we're here to simplify it.

Discover if Hindprakash Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HPIL

Hindprakash Industries

Manufactures and trades in dyes, auxiliaries, intermediates, and chemicals in India and internationally.

Proven track record with slight risk.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets