- India

- /

- Metals and Mining

- /

- NSEI:HINDALCO

Little Excitement Around Hindalco Industries Limited's (NSE:HINDALCO) Earnings

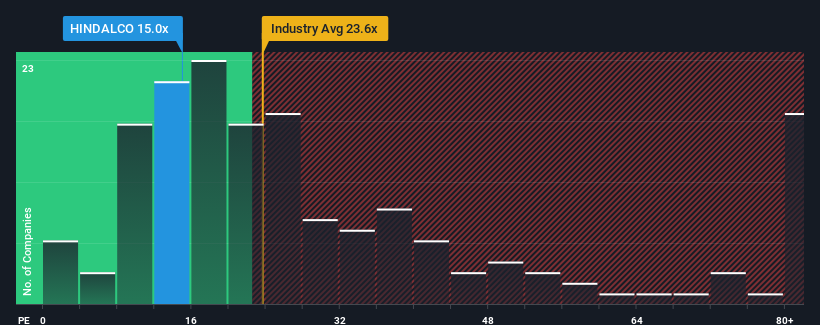

Hindalco Industries Limited's (NSE:HINDALCO) price-to-earnings (or "P/E") ratio of 15x might make it look like a strong buy right now compared to the market in India, where around half of the companies have P/E ratios above 31x and even P/E's above 59x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

While the market has experienced earnings growth lately, Hindalco Industries' earnings have gone into reverse gear, which is not great. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Hindalco Industries

How Is Hindalco Industries' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as depressed as Hindalco Industries' is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered a frustrating 39% decrease to the company's bottom line. Even so, admirably EPS has lifted 186% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 14% per year during the coming three years according to the analysts following the company. Meanwhile, the rest of the market is forecast to expand by 20% per year, which is noticeably more attractive.

In light of this, it's understandable that Hindalco Industries' P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Hindalco Industries' P/E

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Hindalco Industries' analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 3 warning signs for Hindalco Industries that we have uncovered.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Hindalco Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HINDALCO

Hindalco Industries

Produces and sells aluminum and copper products in India and internationally.

Flawless balance sheet with solid track record and pays a dividend.