Advertisement

- India

- /

- Paper and Forestry Products

- /

- NSEI:GREENPANEL

Greenpanel Industries Limited (NSE:GREENPANEL) Just Reported Third-Quarter Earnings And Analysts Are Lifting Their Estimates

Greenpanel Industries Limited (NSE:GREENPANEL) came out with its third-quarter results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. Results overall were respectable, with statutory earnings of ₹1.18 per share roughly in line with what the analysts had forecast. Revenues of ₹3.2b came in 3.1% ahead of analyst predictions. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Greenpanel Industries after the latest results.

See our latest analysis for Greenpanel Industries

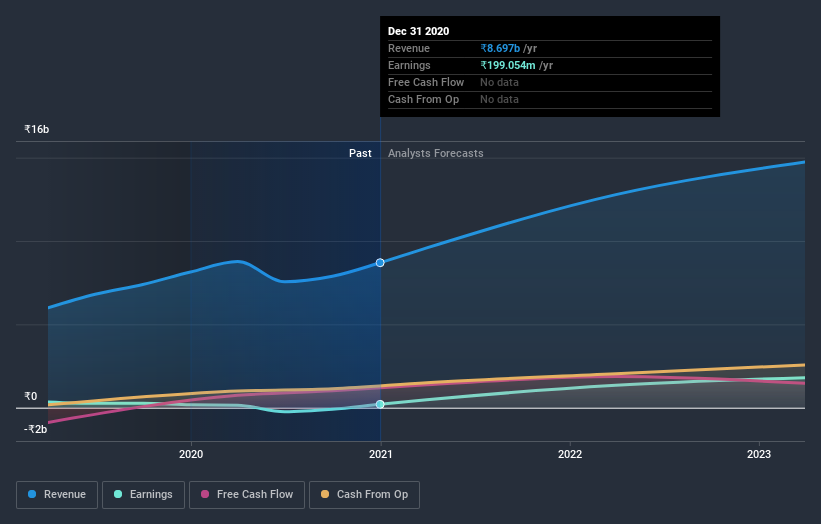

Taking into account the latest results, the consensus forecast from Greenpanel Industries' dual analysts is for revenues of ₹12.8b in 2022, which would reflect a huge 47% improvement in sales compared to the last 12 months. Per-share earnings are expected to jump 573% to ₹11.00. Yet prior to the latest earnings, the analysts had been anticipated revenues of ₹11.6b and earnings per share (EPS) of ₹7.75 in 2022. There has definitely been an improvement in perception after these results, with the analysts noticeably increasing both their earnings and revenue estimates.

With these upgrades, we're not surprised to see that the analysts have lifted their price target 61% to ₹208per share.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The analysts are definitely expecting Greenpanel Industries' growth to accelerate, with the forecast 47% growth ranking favourably alongside historical growth of 6.8% per annum over the past year. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 11% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Greenpanel Industries to grow faster than the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Greenpanel Industries following these results. Happily, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

Before you take the next step you should know about the 3 warning signs for Greenpanel Industries (1 is concerning!) that we have uncovered.

If you decide to trade Greenpanel Industries, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:GREENPANEL

Greenpanel Industries

Engages in the manufacturing, marketing, and sale of plywood, medium density fibre board (MDF), and allied products in India and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor