Advertisement

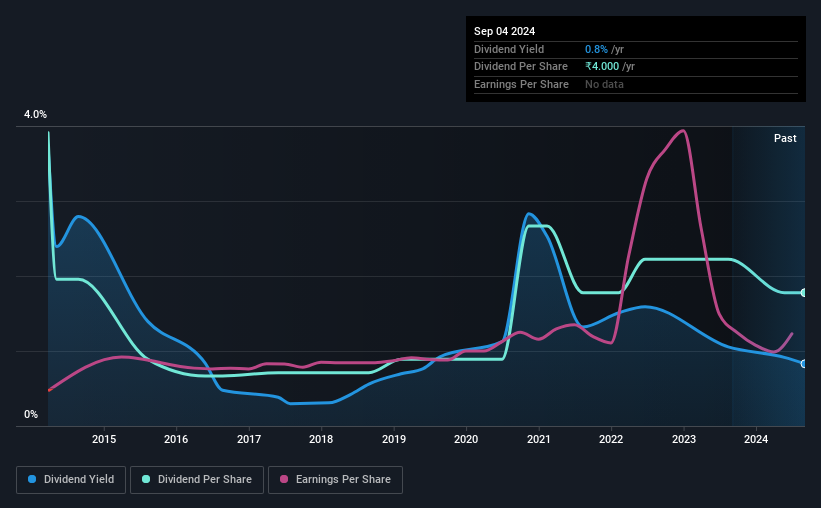

GOCL Corporation Limited (NSE:GOCLCORP) has announced that on 24th of October, it will be paying a dividend of₹4.00, which a reduction from last year's comparable dividend. However, the dividend yield of 0.8% still remains in a typical range for the industry.

Check out our latest analysis for GOCL

GOCL's Payment Has Solid Earnings Coverage

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. The last dividend was quite comfortably covered by GOCL's earnings, but it was a bit tighter on the cash flow front. By paying out so much of its cash flows, this could indicate that the company has limited opportunities for investment and growth.

If the trend of the last few years continues, EPS will grow by 13.5% over the next 12 months. If the dividend continues on this path, the payout ratio could be 25% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2014, the annual payment back then was ₹8.80, compared to the most recent full-year payment of ₹4.00. This works out to be a decline of approximately 7.6% per year over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

The Dividend Looks Likely To Grow

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. GOCL has impressed us by growing EPS at 13% per year over the past five years. Shareholders are getting plenty of the earnings returned to them, which combined with strong growth makes this quite appealing.

In Summary

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. While GOCL is earning enough to cover the dividend, we are generally unimpressed with its future prospects. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Just as an example, we've come across 2 warning signs for GOCL you should be aware of, and 1 of them can't be ignored. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:GOCLCORP

GOCL

Engages in the electronics manufacturing services and the realty businesses in India and internationally.

Proven track record average dividend payer.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor