Advertisement

Why Investors Shouldn't Be Surprised By Gujarat Fluorochemicals Limited's (NSE:FLUOROCHEM) 29% Share Price Surge

Gujarat Fluorochemicals Limited (NSE:FLUOROCHEM) shareholders have had their patience rewarded with a 29% share price jump in the last month. Looking back a bit further, it's encouraging to see the stock is up 38% in the last year.

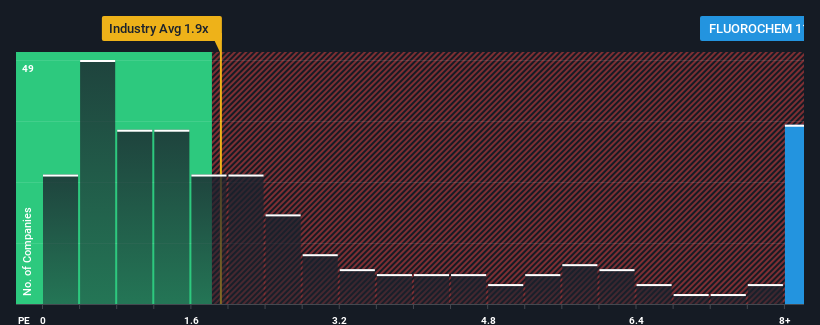

Since its price has surged higher, when almost half of the companies in India's Chemicals industry have price-to-sales ratios (or "P/S") below 1.9x, you may consider Gujarat Fluorochemicals as a stock not worth researching with its 11.1x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Gujarat Fluorochemicals

What Does Gujarat Fluorochemicals' Recent Performance Look Like?

While the industry has experienced revenue growth lately, Gujarat Fluorochemicals' revenue has gone into reverse gear, which is not great. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Gujarat Fluorochemicals.How Is Gujarat Fluorochemicals' Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Gujarat Fluorochemicals' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 24% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 41% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Turning to the outlook, the next year should generate growth of 37% as estimated by the ten analysts watching the company. With the industry only predicted to deliver 16%, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Gujarat Fluorochemicals' P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Gujarat Fluorochemicals' P/S?

Shares in Gujarat Fluorochemicals have seen a strong upwards swing lately, which has really helped boost its P/S figure. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Gujarat Fluorochemicals maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Chemicals industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Before you settle on your opinion, we've discovered 1 warning sign for Gujarat Fluorochemicals that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:FLUOROCHEM

Gujarat Fluorochemicals

Engages in the manufacture and trading of bulk chemicals, refrigerant gases, fluorochemicals, fluoropolymers, and allied activities in India, Europe, the United States, and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.6% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.5% undervalued

AG

Community Contributor