- India

- /

- Paper and Forestry Products

- /

- NSEI:EMAMIPAP

Are Emami Paper Mills Limited's (NSE:EMAMIPAP) Fundamentals Good Enough to Warrant Buying Given The Stock's Recent Weakness?

It is hard to get excited after looking at Emami Paper Mills' (NSE:EMAMIPAP) recent performance, when its stock has declined 13% over the past month. However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. Particularly, we will be paying attention to Emami Paper Mills' ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Put another way, it reveals the company's success at turning shareholder investments into profits.

View our latest analysis for Emami Paper Mills

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Emami Paper Mills is:

6.1% = ₹493m ÷ ₹8.1b (Based on the trailing twelve months to December 2024).

The 'return' is the yearly profit. One way to conceptualize this is that for each ₹1 of shareholders' capital it has, the company made ₹0.06 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Emami Paper Mills' Earnings Growth And 6.1% ROE

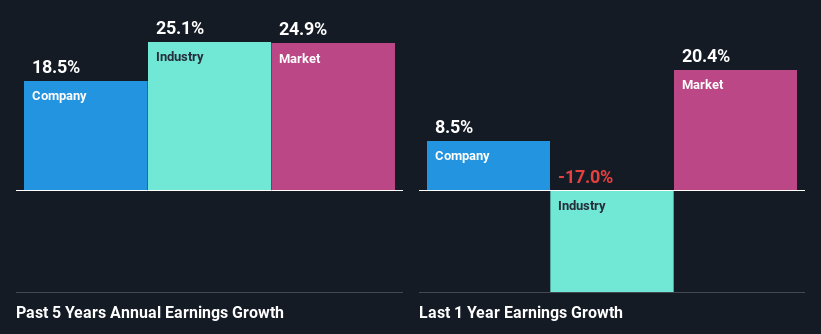

It is quite clear that Emami Paper Mills' ROE is rather low. A comparison with the industry shows that the company's ROE is pretty similar to the average industry ROE of 7.0%. However, the modest 19% net income growth seen by Emami Paper Mills over the past five years is a positive sign. We reckon that there could also be other factors at play that are influencing the company's growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

We then compared Emami Paper Mills' net income growth with the industry and found that the company's growth figure is lower than the average industry growth rate of 25% in the same 5-year period, which is a bit concerning.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Emami Paper Mills fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Emami Paper Mills Making Efficient Use Of Its Profits?

Emami Paper Mills has a low three-year median payout ratio of 12%, meaning that the company retains the remaining 88% of its profits. This suggests that the management is reinvesting most of the profits to grow the business.

Moreover, Emami Paper Mills is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years.

Conclusion

Overall, we feel that Emami Paper Mills certainly does have some positive factors to consider. Namely, its respectable earnings growth, which it achieved due to it retaining most of its profits. However, given the low ROE, investors may not be benefitting from all that reinvestment after all. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. Our risks dashboard would have the 3 risks we have identified for Emami Paper Mills.

If you're looking to trade Emami Paper Mills, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Emami Paper Mills might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:EMAMIPAP

Emami Paper Mills

Manufactures and sells paper and paper board products in India.

Established dividend payer and good value.

Similar Companies

Market Insights

Community Narratives