Advertisement

Is DMCC Speciality Chemicals Limited's (NSE:DMCC) Recent Price Movement Underpinned By Its Weak Fundamentals?

With its stock down 29% over the past three months, it is easy to disregard DMCC Speciality Chemicals (NSE:DMCC). We, however decided to study the company's financials to determine if they have got anything to do with the price decline. Long-term fundamentals are usually what drive market outcomes, so it's worth paying close attention. Specifically, we decided to study DMCC Speciality Chemicals' ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for DMCC Speciality Chemicals is:

9.8% = ₹208m ÷ ₹2.1b (Based on the trailing twelve months to December 2024).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each ₹1 of shareholders' capital it has, the company made ₹0.10 in profit.

View our latest analysis for DMCC Speciality Chemicals

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of DMCC Speciality Chemicals' Earnings Growth And 9.8% ROE

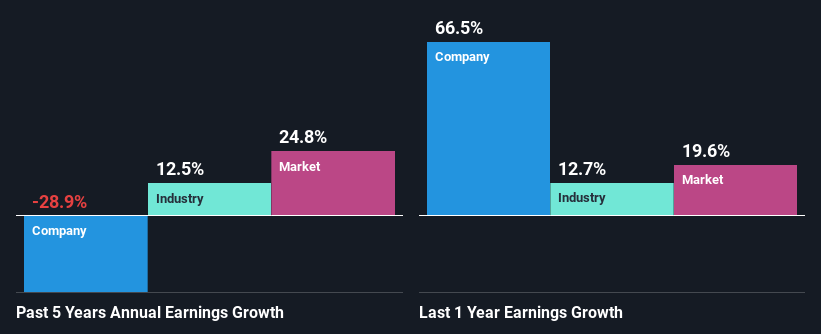

On the face of it, DMCC Speciality Chemicals' ROE is not much to talk about. However, given that the company's ROE is similar to the average industry ROE of 10%, we may spare it some thought. Having said that, DMCC Speciality Chemicals' five year net income decline rate was 29%. Remember, the company's ROE is a bit low to begin with. Therefore, the decline in earnings could also be the result of this.

However, when we compared DMCC Speciality Chemicals' growth with the industry we found that while the company's earnings have been shrinking, the industry has seen an earnings growth of 13% in the same period. This is quite worrisome.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about DMCC Speciality Chemicals''s valuation, check out this gauge of its price-to-earnings ratio , as compared to its industry.

Is DMCC Speciality Chemicals Using Its Retained Earnings Effectively?

DMCC Speciality Chemicals' low three-year median payout ratio of 12% (or a retention ratio of 88%) over the last three years should mean that the company is retaining most of its earnings to fuel its growth but the company's earnings have actually shrunk. The low payout should mean that the company is retaining most of its earnings and consequently, should see some growth. So there could be some other explanations in that regard. For example, the company's business may be deteriorating.

In addition, DMCC Speciality Chemicals has been paying dividends over a period of seven years suggesting that keeping up dividend payments is preferred by the management even though earnings have been in decline.

Summary

In total, we're a bit ambivalent about DMCC Speciality Chemicals' performance. While the company does have a high rate of profit retention, its low rate of return is probably hampering its earnings growth. Wrapping up, we would proceed with caution with this company and one way of doing that would be to look at the risk profile of the business. To know the 4 risks we have identified for DMCC Speciality Chemicals visit our risks dashboard for free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:DMCC

DMCC Speciality Chemicals

Manufactures and sells specialty and commodity chemicals in India and internationally.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|37.1% undervalued

UN

Community Contributor