Advertisement

New India Assurance's (NSE:NIACL) Dividend Is Being Reduced To ₹1.80

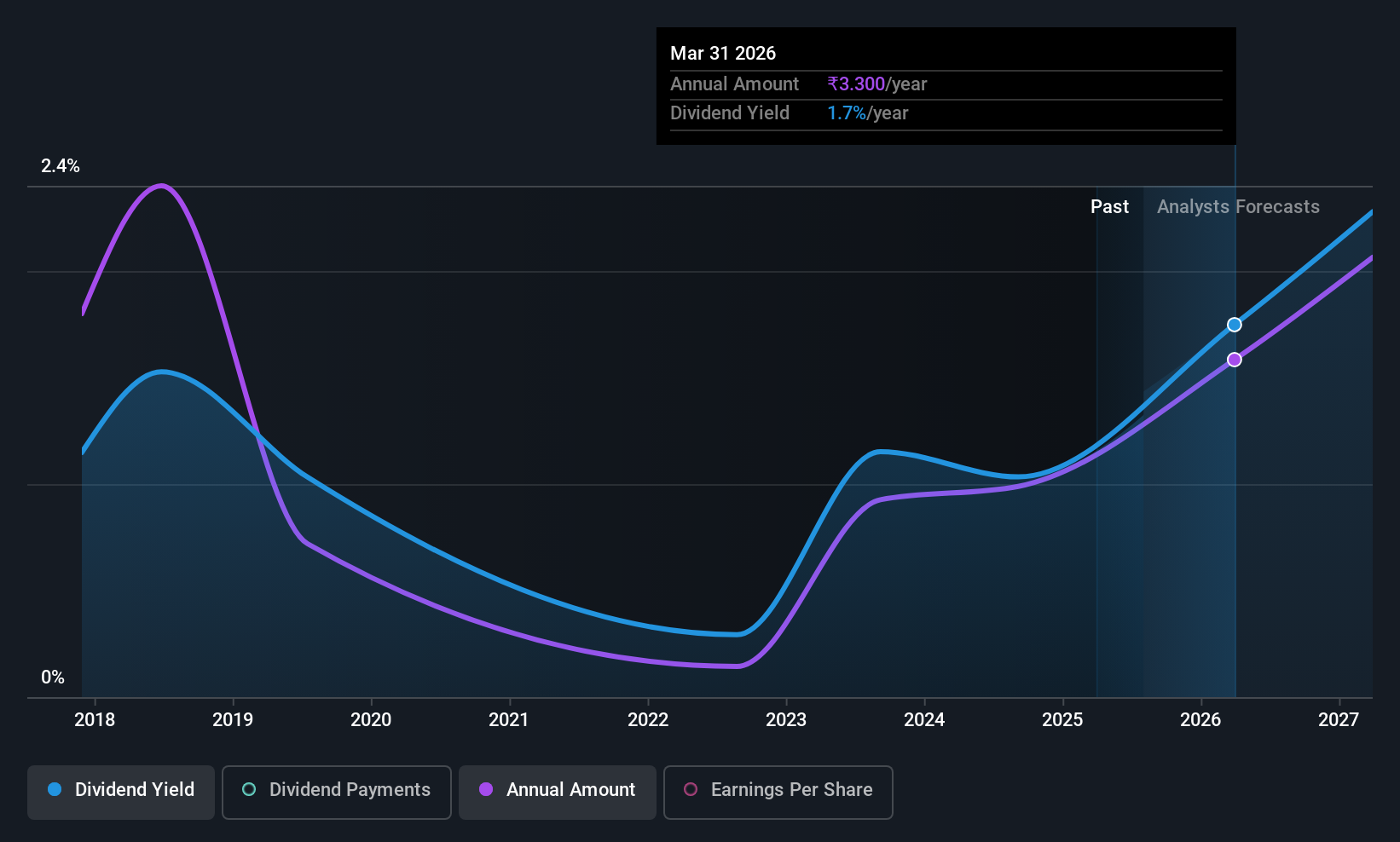

The New India Assurance Company Limited (NSE:NIACL) has announced that on 1st of January, it will be paying a dividend of₹1.80, which a reduction from last year's comparable dividend. This means the annual payment is 1.0% of the current stock price, which is above the average for the industry.

New India Assurance's Projected Earnings Seem Likely To Cover Future Distributions

A big dividend yield for a few years doesn't mean much if it can't be sustained. Based on the last payment, New India Assurance was earning enough to cover the dividend, but free cash flows weren't positive. We think that cash flows should take priority over earnings, so this is definitely a worry for the dividend going forward.

The next year is set to see EPS grow by 23.0%. If the dividend continues along recent trends, we estimate the payout ratio will be 20%, which is in the range that makes us comfortable with the sustainability of the dividend.

See our latest analysis for New India Assurance

New India Assurance's Dividend Has Lacked Consistency

Looking back, New India Assurance's dividend hasn't been particularly consistent. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2017, the annual payment back then was ₹3.75, compared to the most recent full-year payment of ₹1.80. This works out to be a decline of approximately 8.8% per year over that time. A company that decreases its dividend over time generally isn't what we are looking for.

New India Assurance May Find It Hard To Grow The Dividend

Given that the track record hasn't been stellar, we really want to see earnings per share growing over time. It's not great to see that New India Assurance's earnings per share has fallen at approximately 4.2% per year over the past five years. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends. Earnings are predicted to grow over the next year, but we would remain cautious until a track record of earnings growth is established.

The Dividend Could Prove To Be Unreliable

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. While New India Assurance is earning enough to cover the payments, the cash flows are lacking. This company is not in the top tier of income providing stocks.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 1 warning sign for New India Assurance that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if New India Assurance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NIACL

New India Assurance

Operates as a general insurance company in India and internationally.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|6.3% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.8% undervalued

GM

Community Contributor