Advertisement

Does Bombay Super Hybrid Seeds (NSE:BSHSL) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Bombay Super Hybrid Seeds Limited (NSE:BSHSL) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

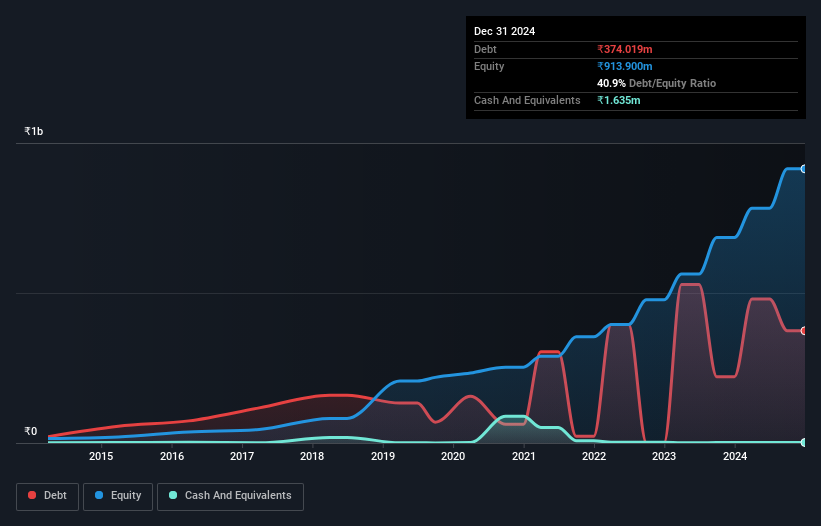

See our latest analysis for Bombay Super Hybrid Seeds

What Is Bombay Super Hybrid Seeds's Net Debt?

As you can see below, at the end of September 2024, Bombay Super Hybrid Seeds had ₹374.0m of debt, up from ₹220.9m a year ago. Click the image for more detail. Net debt is about the same, since the it doesn't have much cash.

How Healthy Is Bombay Super Hybrid Seeds' Balance Sheet?

According to the last reported balance sheet, Bombay Super Hybrid Seeds had liabilities of ₹692.4m due within 12 months, and liabilities of ₹16.5m due beyond 12 months. Offsetting this, it had ₹1.64m in cash and ₹547.5m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹159.7m.

Having regard to Bombay Super Hybrid Seeds' size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the ₹14.9b company is struggling for cash, we still think it's worth monitoring its balance sheet.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Bombay Super Hybrid Seeds's low debt to EBITDA ratio of 1.2 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 6.2 times last year does give us pause. But the interest payments are certainly sufficient to have us thinking about how affordable its debt is. Fortunately, Bombay Super Hybrid Seeds grew its EBIT by 8.4% in the last year, making that debt load look even more manageable. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Bombay Super Hybrid Seeds will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, Bombay Super Hybrid Seeds's free cash flow amounted to 24% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Both Bombay Super Hybrid Seeds's ability to handle its debt, based on its EBITDA, and its level of total liabilities gave us comfort that it can handle its debt. On the other hand, its conversion of EBIT to free cash flow makes us a little less comfortable about its debt. When we consider all the elements mentioned above, it seems to us that Bombay Super Hybrid Seeds is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for Bombay Super Hybrid Seeds that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Bombay Super Hybrid Seeds might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BSHSL

Bombay Super Hybrid Seeds

Engages in the research, production, processing, and marketing of hybrid and GM seeds in India.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.2% undervalued

TO

Community Contributor