Advertisement

- India

- /

- Capital Markets

- /

- NSEI:UTIAMC

UTI Asset Management's (NSE:UTIAMC) Dividend Will Be Increased To ₹22.00

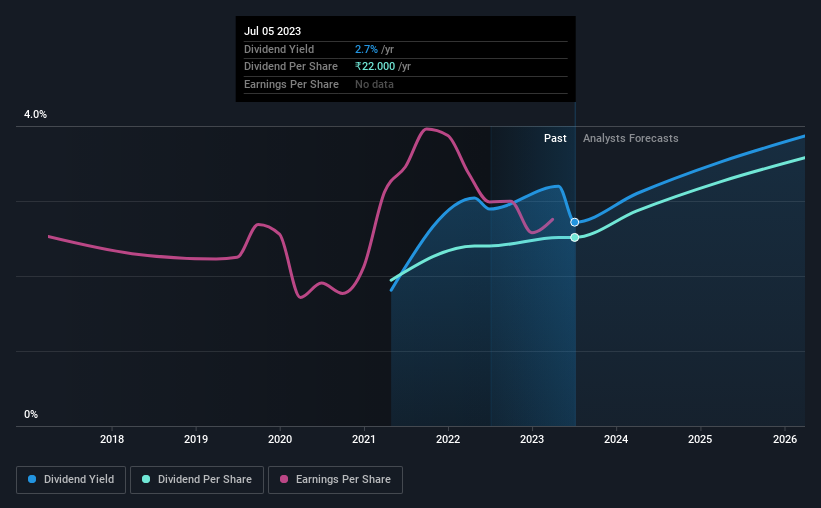

The board of UTI Asset Management Company Limited (NSE:UTIAMC) has announced that it will be paying its dividend of ₹22.00 on the 28th of July, an increased payment from last year's comparable dividend. This makes the dividend yield 2.7%, which is above the industry average.

Check out our latest analysis for UTI Asset Management

UTI Asset Management's Earnings Easily Cover The Distributions

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Based on the last dividend, UTI Asset Management is earning enough to cover the payment, but then it makes up 98% of cash flows. This signals that the company is more focused on returning cash flow to shareholders, but it could mean that the dividend is exposed to cuts in the future.

The next year is set to see EPS grow by 48.3%. If the dividend continues on this path, the payout ratio could be 59% by next year, which we think can be pretty sustainable going forward.

UTI Asset Management Is Still Building Its Track Record

The company has maintained a consistent dividend for a few years now, but we would like to see a longer track record before relying on it. Since 2021, the dividend has gone from ₹17.00 total annually to ₹22.00. This implies that the company grew its distributions at a yearly rate of about 14% over that duration. UTI Asset Management has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

Dividend Growth May Be Hard To Achieve

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Earnings per share has been crawling upwards at 3.7% per year. Growth of 3.7% per annum is not particularly high, which might explain why the company is paying out a higher proportion of earnings. This isn't bad in itself, but unless earnings growth pick up we wouldn't expect dividends to grow either.

In Summary

In summary, while it's always good to see the dividend being raised, we don't think UTI Asset Management's payments are rock solid. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 1 warning sign for UTI Asset Management that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:UTIAMC

UTI Asset Management

UTI Asset Management Company (P) Ltd. is a privately owned investment manager.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor