Advertisement

- India

- /

- Healthcare Services

- /

- NSEI:APOLLOHOSP

Indian Exchange Growth Companies With At Least 10% Insider Ownership

Simply Wall St

Reviewed by Simply Wall St

The Indian market has shown robust performance, rising 2.4% in the last week and an impressive 46% over the past year, with earnings expected to grow by 16% annually. In such a thriving environment, stocks of growth companies with high insider ownership can be particularly appealing as they often indicate confidence from those who know the company best.

Top 10 Growth Companies With High Insider Ownership In India

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 28.9% |

| Kirloskar Pneumatic (BSE:505283) | 30.6% | 29.8% |

| Pitti Engineering (BSE:513519) | 33.6% | 28.0% |

| Shivalik Bimetal Controls (BSE:513097) | 19.5% | 28.7% |

| Jupiter Wagons (NSEI:JWL) | 11.1% | 27.2% |

| Rajratan Global Wire (BSE:517522) | 19.8% | 33.5% |

| Dixon Technologies (India) (NSEI:DIXON) | 24.9% | 33.7% |

| Paisalo Digital (BSE:532900) | 16.3% | 23.8% |

| JNK India (NSEI:JNKINDIA) | 23.8% | 31.8% |

| Aether Industries (NSEI:AETHER) | 31.1% | 39.8% |

Below we spotlight a couple of our favorites from our exclusive screener.

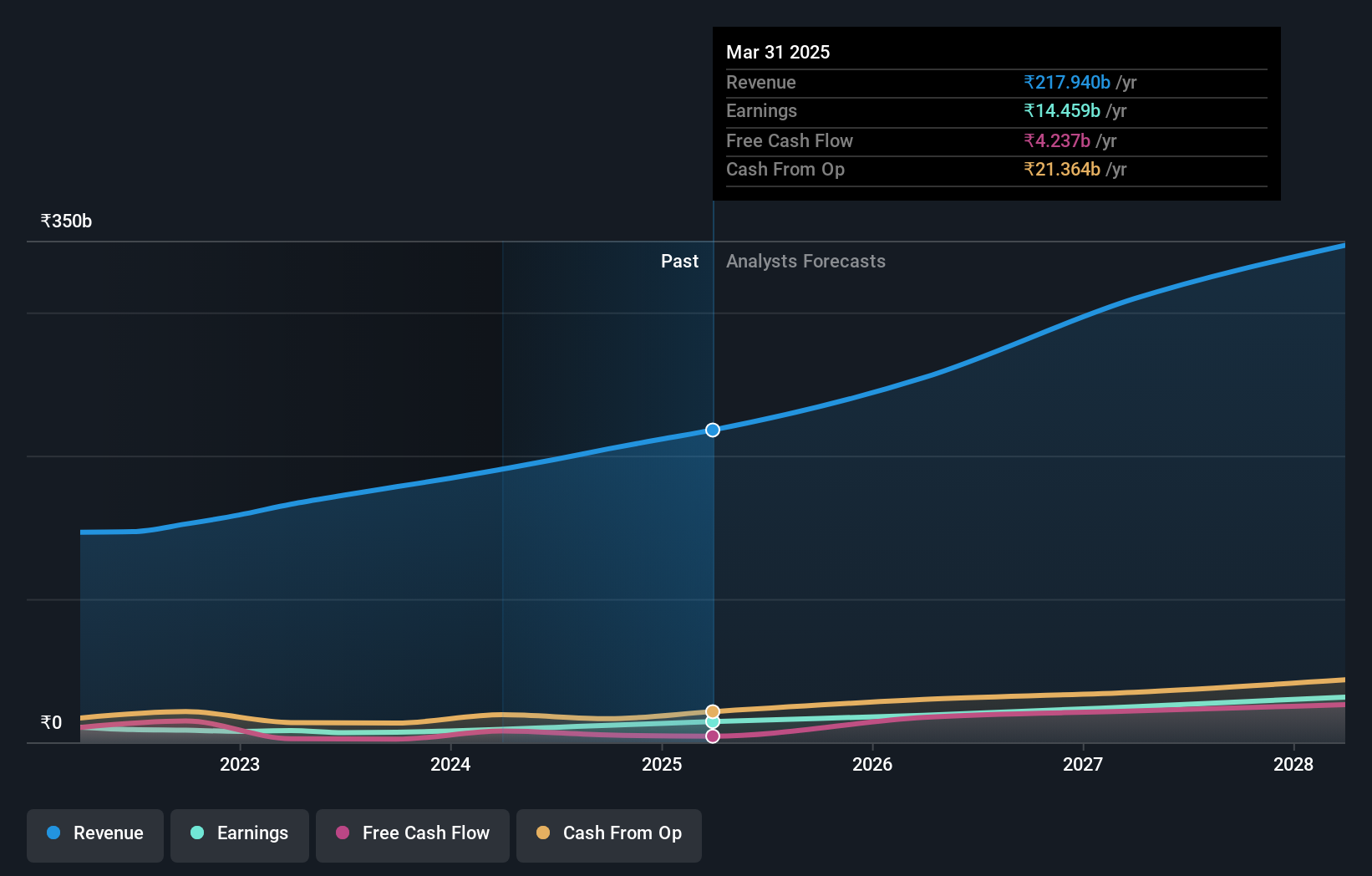

Apollo Hospitals Enterprise (NSEI:APOLLOHOSP)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Apollo Hospitals Enterprise Limited operates a network of healthcare services both in India and internationally, with a market capitalization of approximately ₹90.84 billion.

Operations: The company generates revenue primarily through Healthcare Services (₹99.39 billion), Retail Health & Diagnostics (₹13.64 billion), and Digital Health & Pharmacy Distribution (₹78.27 billion).

Insider Ownership: 10.4%

Apollo Hospitals Enterprise, with high insider ownership, reflects robust growth potential amid India's expanding healthcare sector. Recently expressing interest in acquiring Jaypee Healthcare, Apollo aims to enhance its market footprint. The company has shown strong financial performance with a notable increase in annual revenue to INR 191.66 billion and net income of INR 8.99 billion for FY2024. Forecasted earnings growth at 33.2% annually outpaces the broader Indian market projection of 15.8%. This is complemented by strategic leadership adjustments focusing on digital health expansion, underscoring a proactive approach to evolving consumer needs in healthcare services.

- Take a closer look at Apollo Hospitals Enterprise's potential here in our earnings growth report.

- Upon reviewing our latest valuation report, Apollo Hospitals Enterprise's share price might be too optimistic.

Kalpataru Projects International (NSEI:KPIL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kalpataru Projects International Limited, with a market capitalization of ₹206.74 billion, specializes in providing engineering, procurement, and construction (EPC) services across various sectors including power transmission and distribution, buildings and factories, water, railways, oil and gas, and urban infrastructure both in India and globally.

Operations: Kalpataru Projects International Limited generates revenue primarily through its Development Projects and Engineering, Procurement and Construction (EPC) services, contributing ₹2.80 billion and ₹191.48 billion respectively.

Insider Ownership: 13.4%

Kalpataru Projects International Limited (KPIL) showcases a mixed financial landscape with its earnings expected to grow significantly by 26.89% annually over the next three years, outpacing the Indian market's forecasted 15.8% growth. Despite this promising growth in earnings, KPIL's revenue growth projection of 12.5% annually is modest compared to high-growth benchmarks. Additionally, KPIL faces challenges with interest payments not well covered by earnings and an unstable dividend track record, which may concern investors focused on financial stability and consistent returns. Recent strategic moves include securing new orders worth INR 23.33 billion across various sectors and addressing debt optimization through non-convertible debentures issuance and prepayments, indicating proactive management in strengthening its financial position and business expansion.

- Delve into the full analysis future growth report here for a deeper understanding of Kalpataru Projects International.

- Our valuation report here indicates Kalpataru Projects International may be overvalued.

One97 Communications (NSEI:PAYTM)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: One97 Communications Limited, operating under the brand Paytm, offers payment, commerce and cloud, and financial services in India with a market capitalization of approximately ₹300.54 billion.

Operations: The company generates revenue primarily through data processing services, totaling ₹99.78 billion.

Insider Ownership: 19.5%

One97 Communications Limited (Paytm) is poised for notable growth with earnings expected to surge by 60.05% annually. Despite slower revenue growth at 9.9% per year, it outpaces the broader Indian market's 9.7%. Paytm's recent strategic initiative includes launching 'Paytm Health Saathi,' enhancing support for its merchant network by offering affordable healthcare and income protection plans, starting from just INR 35 per month, reflecting its commitment to stakeholder welfare and business continuity amidst discussions of divesting its events and movie ticketing business to Zomato.

- Unlock comprehensive insights into our analysis of One97 Communications stock in this growth report.

- Our expertly prepared valuation report One97 Communications implies its share price may be lower than expected.

Taking Advantage

- Explore the 84 names from our Fast Growing Indian Companies With High Insider Ownership screener here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:APOLLOHOSP

Apollo Hospitals Enterprise

Engages in the provision of healthcare services in India and internationally.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor