Advertisement

- India

- /

- Capital Markets

- /

- NSEI:NAGREEKCAP

Here's Why Nagreeka Capital & Infrastructure (NSE:NAGREEKCAP) Has Caught The Eye Of Investors

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Nagreeka Capital & Infrastructure (NSE:NAGREEKCAP). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Nagreeka Capital & Infrastructure with the means to add long-term value to shareholders.

Check out our latest analysis for Nagreeka Capital & Infrastructure

How Fast Is Nagreeka Capital & Infrastructure Growing Its Earnings Per Share?

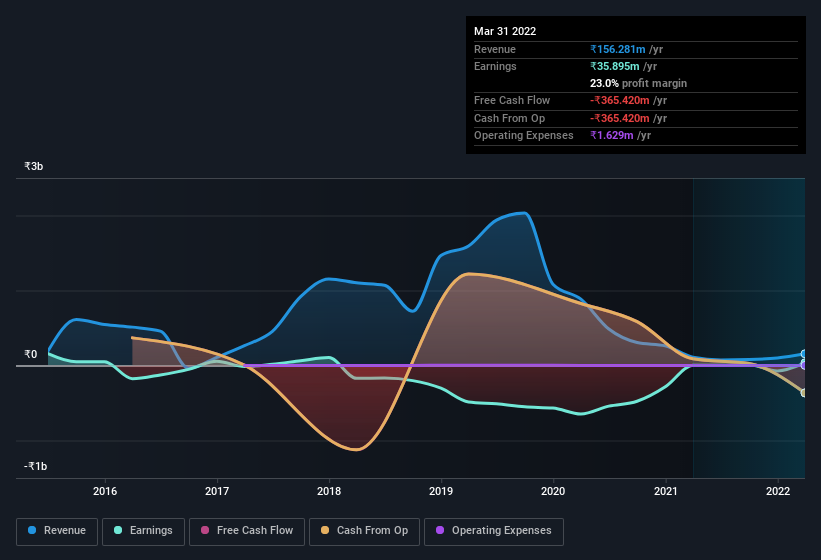

Strong earnings per share (EPS) results are an indicator of a company achieving solid profits, which investors look upon favourably and so the share price tends to reflect great EPS performance. So for many budding investors, improving EPS is considered a good sign. It's an outstanding feat for Nagreeka Capital & Infrastructure to have grown EPS from ₹0.14 to ₹2.85 in just one year. When you see earnings grow that quickly, it often means good things ahead for the company. This could point to the business hitting a point of inflection.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. Our analysis has highlighted that Nagreeka Capital & Infrastructure's revenue from operations did not account for all of their revenue in the previous 12 months, so our analysis of its margins might not accurately reflect the underlying business. Nagreeka Capital & Infrastructure shareholders can take confidence from the fact that EBIT margins are up from 55% to 80%, and revenue is growing. That's great to see, on both counts.

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

Since Nagreeka Capital & Infrastructure is no giant, with a market capitalisation of ₹151m, you should definitely check its cash and debt before getting too excited about its prospects.

Are Nagreeka Capital & Infrastructure Insiders Aligned With All Shareholders?

Theory would suggest that it's an encouraging sign to see high insider ownership of a company, since it ties company performance directly to the financial success of its management. So we're pleased to report that Nagreeka Capital & Infrastructure insiders own a meaningful share of the business. Owning 36% of the company, insiders have plenty riding on the performance of the the share price. This should be a welcoming sign for investors because it suggests that the people making the decisions are also impacted by their choices. Valued at only ₹151m Nagreeka Capital & Infrastructure is really small for a listed company. That means insiders only have ₹55m worth of shares, despite the large proportional holding. That's not a huge stake in absolute terms, but it should help keep insiders aligned with other shareholders.

Should You Add Nagreeka Capital & Infrastructure To Your Watchlist?

Nagreeka Capital & Infrastructure's earnings have taken off in quite an impressive fashion. That EPS growth certainly is attention grabbing, and the large insider ownership only serves to further stoke our interest. The hope is, of course, that the strong growth marks a fundamental improvement in the business economics. So based on this quick analysis, we do think it's worth considering Nagreeka Capital & Infrastructure for a spot on your watchlist. Even so, be aware that Nagreeka Capital & Infrastructure is showing 5 warning signs in our investment analysis , and 3 of those make us uncomfortable...

Although Nagreeka Capital & Infrastructure certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see insider buying, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Nagreeka Capital & Infrastructure might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NAGREEKCAP

Proven track record and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.5% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.3% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.3% undervalued

AG

Community Contributor