Advertisement

- India

- /

- Capital Markets

- /

- NSEI:CARERATING

CARE Ratings Limited's (NSE:CARERATING) 35% Share Price Surge Not Quite Adding Up

CARE Ratings Limited (NSE:CARERATING) shares have had a really impressive month, gaining 35% after a shaky period beforehand. Looking back a bit further, it's encouraging to see the stock is up 38% in the last year.

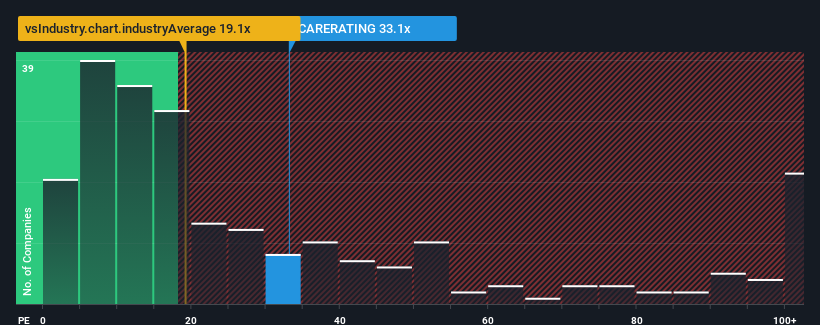

Since its price has surged higher, CARE Ratings may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 33.1x, since almost half of all companies in India have P/E ratios under 26x and even P/E's lower than 15x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Our free stock report includes 1 warning sign investors should be aware of before investing in CARE Ratings. Read for free now.With earnings growth that's superior to most other companies of late, CARE Ratings has been doing relatively well. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for CARE Ratings

Is There Enough Growth For CARE Ratings?

In order to justify its P/E ratio, CARE Ratings would need to produce impressive growth in excess of the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 36% last year. The strong recent performance means it was also able to grow EPS by 80% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the sole analyst covering the company suggest earnings should grow by 17% over the next year. With the market predicted to deliver 24% growth , the company is positioned for a weaker earnings result.

With this information, we find it concerning that CARE Ratings is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

CARE Ratings shares have received a push in the right direction, but its P/E is elevated too. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that CARE Ratings currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

It is also worth noting that we have found 1 warning sign for CARE Ratings that you need to take into consideration.

If you're unsure about the strength of CARE Ratings' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:CARERATING

CARE Ratings

A credit rating agency, provides various rating and related services in India and internationally.

Flawless balance sheet with reasonable growth potential and pays a dividend.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor