Advertisement

- India

- /

- Hospitality

- /

- NSEI:WESTLIFE

Westlife Foodworld Limited (NSE:WESTLIFE) Stock's Been Sliding But Fundamentals Look Decent: Will The Market Correct The Share Price In The Future?

With its stock down 17% over the past three months, it is easy to disregard Westlife Foodworld (NSE:WESTLIFE). However, stock prices are usually driven by a company’s financials over the long term, which in this case look pretty respectable. In this article, we decided to focus on Westlife Foodworld's ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Westlife Foodworld is:

6.0% = ₹375m ÷ ₹6.2b (Based on the trailing twelve months to September 2025).

The 'return' is the profit over the last twelve months. That means that for every ₹1 worth of shareholders' equity, the company generated ₹0.06 in profit.

Check out our latest analysis for Westlife Foodworld

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Westlife Foodworld's Earnings Growth And 6.0% ROE

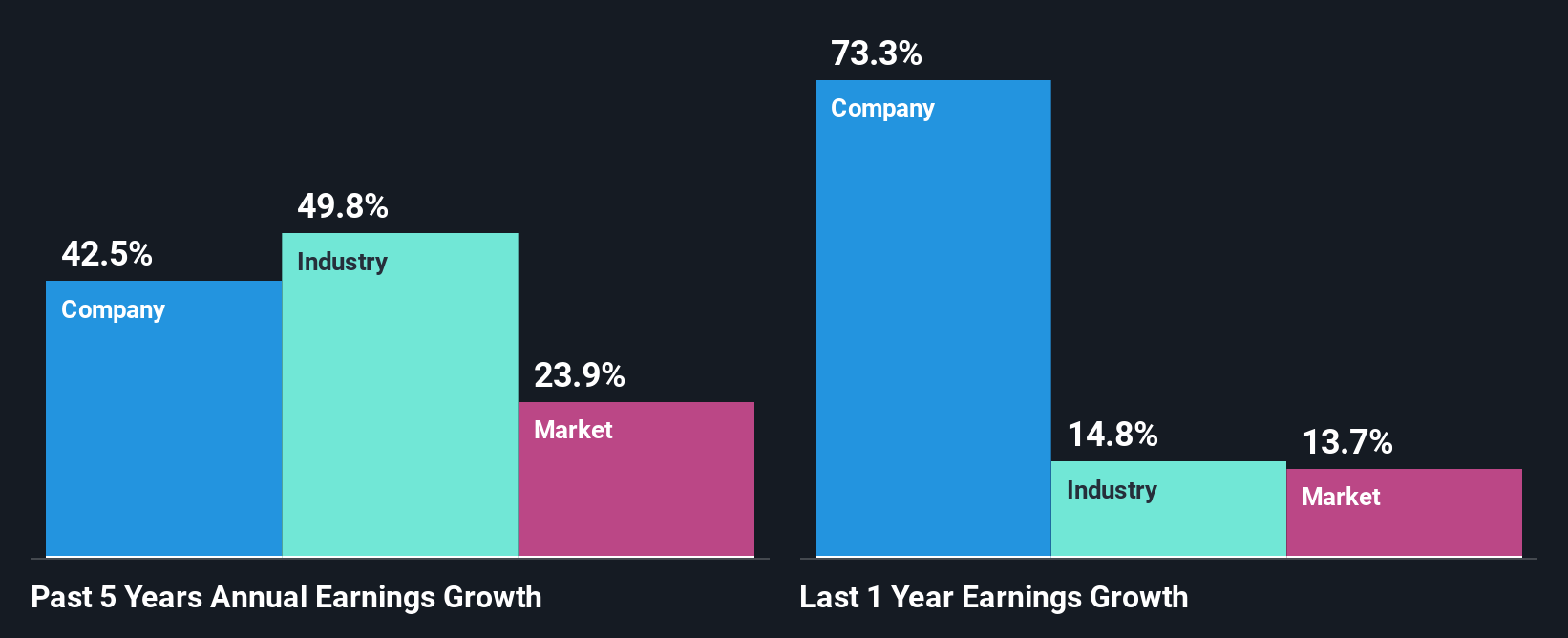

It is quite clear that Westlife Foodworld's ROE is rather low. Even when compared to the industry average of 8.9%, the ROE figure is pretty disappointing. However, we we're pleasantly surprised to see that Westlife Foodworld grew its net income at a significant rate of 43% in the last five years. We believe that there might be other aspects that are positively influencing the company's earnings growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

As a next step, we compared Westlife Foodworld's net income growth with the industry and found that the company has a similar growth figure when compared with the industry average growth rate of 50% in the same period.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Westlife Foodworld fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Westlife Foodworld Efficiently Re-investing Its Profits?

Westlife Foodworld's significant three-year median payout ratio of 64% (where it is retaining only 36% of its income) suggests that the company has been able to achieve a high growth in earnings despite returning most of its income to shareholders.

Along with seeing a growth in earnings, Westlife Foodworld only recently started paying dividends. Its quite possible that the company was looking to impress its shareholders. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 24% over the next three years. Accordingly, the expected drop in the payout ratio explains the expected increase in the company's ROE to 16%, over the same period.

Summary

On the whole, we do feel that Westlife Foodworld has some positive attributes. Namely, its high earnings growth. We do however feel that the earnings growth number could have been even higher, had the company been reinvesting more of its earnings and paid out less dividends. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Valuation is complex, but we're here to simplify it.

Discover if Westlife Foodworld might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:WESTLIFE

Westlife Foodworld

Through its subsidiary, Hardcastle Restaurants Private Limited, owns and operates a chain of McDonald's restaurants in Western and Southern India.

Solid track record and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor