- India

- /

- Hospitality

- /

- NSEI:VHLTD

The Market Lifts Viceroy Hotels Limited (NSE:VHLTD) Shares 27% But It Can Do More

Viceroy Hotels Limited (NSE:VHLTD) shares have had a really impressive month, gaining 27% after a shaky period beforehand. But the last month did very little to improve the 100% share price decline over the last year.

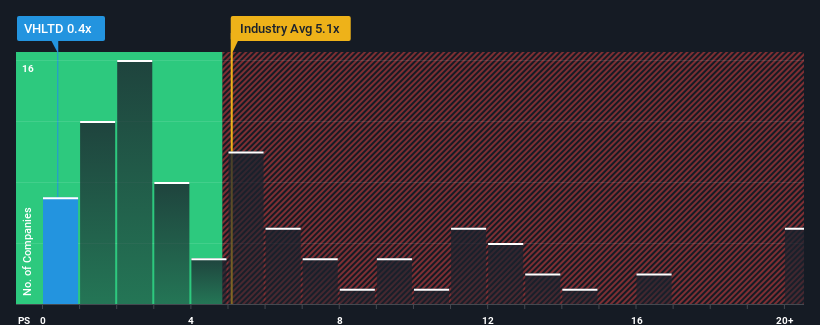

Although its price has surged higher, Viceroy Hotels' price-to-sales (or "P/S") ratio of 0.4x might still make it look like a strong buy right now compared to the wider Hospitality industry in India, where around half of the companies have P/S ratios above 5.1x and even P/S above 10x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

Check out our latest analysis for Viceroy Hotels

How Has Viceroy Hotels Performed Recently?

Revenue has risen firmly for Viceroy Hotels recently, which is pleasing to see. Perhaps the market is expecting this acceptable revenue performance to take a dive, which has kept the P/S suppressed. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

Although there are no analyst estimates available for Viceroy Hotels, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For Viceroy Hotels?

The only time you'd be truly comfortable seeing a P/S as depressed as Viceroy Hotels' is when the company's growth is on track to lag the industry decidedly.

Retrospectively, the last year delivered an exceptional 28% gain to the company's top line. Pleasingly, revenue has also lifted 137% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

When compared to the industry's one-year growth forecast of 28%, the most recent medium-term revenue trajectory is noticeably more alluring

With this information, we find it odd that Viceroy Hotels is trading at a P/S lower than the industry. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Bottom Line On Viceroy Hotels' P/S

Even after such a strong price move, Viceroy Hotels' P/S still trails the rest of the industry. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We're very surprised to see Viceroy Hotels currently trading on a much lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. When we see strong revenue with faster-than-industry growth, we assume there are some significant underlying risks to the company's ability to make money which is applying downwards pressure on the P/S ratio. At least price risks look to be very low if recent medium-term revenue trends continue, but investors seem to think future revenue could see a lot of volatility.

Don't forget that there may be other risks. For instance, we've identified 5 warning signs for Viceroy Hotels that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:VHLTD

Excellent balance sheet and good value.

Market Insights

Community Narratives