Advertisement

- India

- /

- Communications

- /

- NSEI:VINDHYATEL

Exploring Undiscovered Gems In India's Stock Market July 2024

Simply Wall St

Reviewed by Simply Wall St

Over the past year, India's stock market has surged by 45%, though it has remained flat in the last 7 days. With earnings expected to grow by 16% annually, investors might find potential in lesser-known stocks that could benefit from these broader market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In India

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Kokuyo Camlin | 21.96% | 11.97% | 59.14% | ★★★★★★ |

| Le Travenues Technology | 8.99% | 36.48% | 63.83% | ★★★★★★ |

| NGL Fine-Chem | 12.35% | 15.70% | 9.76% | ★★★★★★ |

| BLS E-Services | NA | 43.93% | 59.81% | ★★★★★★ |

| Knowledge Marine & Engineering Works | 35.48% | 46.55% | 46.96% | ★★★★★★ |

| Force Motors | 23.24% | 17.79% | 29.78% | ★★★★★☆ |

| Nibe | 33.91% | 81.20% | 80.04% | ★★★★★☆ |

| Magadh Sugar & Energy | 85.41% | 6.90% | 11.82% | ★★★★☆☆ |

| Monarch Networth Capital | 32.66% | 30.99% | 50.24% | ★★★★☆☆ |

| Vasa Denticity | 0.11% | 38.86% | 55.93% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

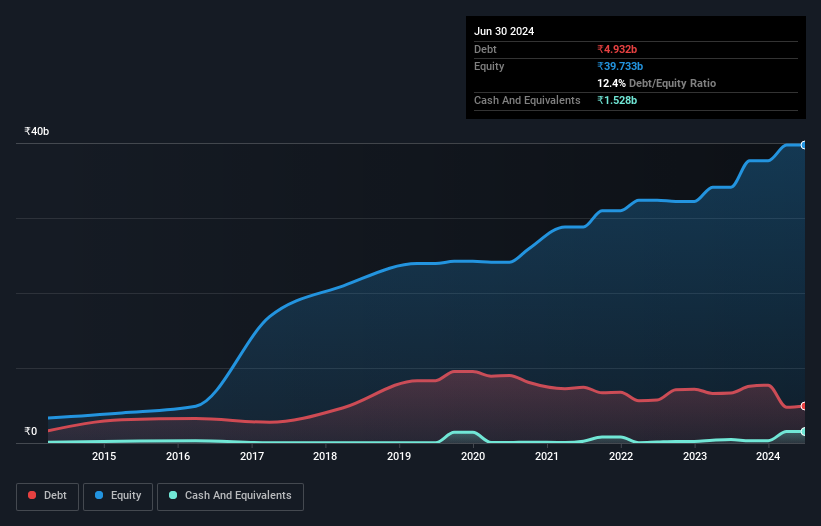

NIIT Learning Systems (NSEI:NIITMTS)

Simply Wall St Value Rating: ★★★★★★

Overview: NIIT Learning Systems Limited, operating as NIIT Managed Training Services, provides managed training services across North America, Europe, Asia, and Oceania with a market capitalization of ₹63.45 billion.

Operations: The company generates revenue primarily through its Education & Training Services, with the most recent figures showing a revenue of ₹15.54 billion. It has achieved a gross profit margin of 51.48% as of the latest reporting period, reflecting its ability to manage cost of goods sold effectively relative to sales.

NIIT Learning Systems, trading below the broader Indian market P/E at 29.8x, showcases robust financial health with earnings growth of 39.7% annually over five years and high-quality earnings. The company's debt is well-managed, evidenced by more cash than total debt and interest payments comfortably covered 10.2 times by EBIT. Recent dividends affirm shareholder value, with a final dividend of INR 2.75 per share following an interim dividend of INR 2.50 last October, signaling confidence in its financial stability and future prospects.

- Unlock comprehensive insights into our analysis of NIIT Learning Systems stock in this health report.

Understand NIIT Learning Systems' track record by examining our Past report.

NIIT Learning Systems (NSEI:NIITMTS)

Simply Wall St Value Rating: ★★★★★★

Overview: NIIT Learning Systems Limited, operating as NIIT Managed Training Services, provides managed training services across North America, Europe, Asia, and Oceania with a market capitalization of ₹63.45 billion.

Operations: The company generates revenue primarily through its Education & Training Services, with the most recent figures showing a revenue of ₹15.54 billion. It has achieved a gross profit margin of 51.48% as of the latest reporting period, reflecting its ability to manage cost of goods sold effectively relative to sales.

NIIT Learning Systems, trading below the broader Indian market P/E at 29.8x, showcases robust financial health with earnings growth of 39.7% annually over five years and high-quality earnings. The company's debt is well-managed, evidenced by more cash than total debt and interest payments comfortably covered 10.2 times by EBIT. Recent dividends affirm shareholder value, with a final dividend of INR 2.75 per share following an interim dividend of INR 2.50 last October, signaling confidence in its financial stability and future prospects.

- Unlock comprehensive insights into our analysis of NIIT Learning Systems stock in this health report.

Understand NIIT Learning Systems' track record by examining our Past report.

S.J.S. Enterprises (NSEI:SJS)

Simply Wall St Value Rating: ★★★★★☆

Overview: S.J.S. Enterprises Limited is a company that specializes in the design, development, manufacturing, sale, and export of decorative aesthetics for the automotive and consumer appliance sectors across both domestic and international markets, with a market capitalization of ₹25.86 billion.

Operations: The company specializes in the manufacturing and selling of self-adhesive labels, generating revenue of ₹6.28 billion as of the latest reported period. It has observed a gross profit margin of 54.62% recently, reflecting its cost management in production processes relative to sales.

S.J.S. Enterprises, a notable player in the Auto Components sector, has demonstrated robust financial health and growth potential. With earnings growth of 26.1% last year, surpassing its industry's 23.2%, the company shows promise beyond its current market recognition. Its Price-To-Earnings ratio stands at an appealing 30.5x, below the Indian market average of 34.1x, suggesting good value. Additionally, S.J.S.'s net debt to equity ratio is a low 3.5%, reflecting prudent financial management amidst a competitive landscape.

- Click here and access our complete health analysis report to understand the dynamics of S.J.S. Enterprises.

Gain insights into S.J.S. Enterprises' past trends and performance with our Past report.

S.J.S. Enterprises (NSEI:SJS)

Simply Wall St Value Rating: ★★★★★☆

Overview: S.J.S. Enterprises Limited is a company that specializes in the design, development, manufacturing, sale, and export of decorative aesthetics for the automotive and consumer appliance sectors across both domestic and international markets, with a market capitalization of ₹25.86 billion.

Operations: The company specializes in the manufacturing and selling of self-adhesive labels, generating revenue of ₹6.28 billion as of the latest reported period. It has observed a gross profit margin of 54.62% recently, reflecting its cost management in production processes relative to sales.

S.J.S. Enterprises, a notable player in the Auto Components sector, has demonstrated robust financial health and growth potential. With earnings growth of 26.1% last year, surpassing its industry's 23.2%, the company shows promise beyond its current market recognition. Its Price-To-Earnings ratio stands at an appealing 30.5x, below the Indian market average of 34.1x, suggesting good value. Additionally, S.J.S.'s net debt to equity ratio is a low 3.5%, reflecting prudent financial management amidst a competitive landscape.

- Click here and access our complete health analysis report to understand the dynamics of S.J.S. Enterprises.

Gain insights into S.J.S. Enterprises' past trends and performance with our Past report.

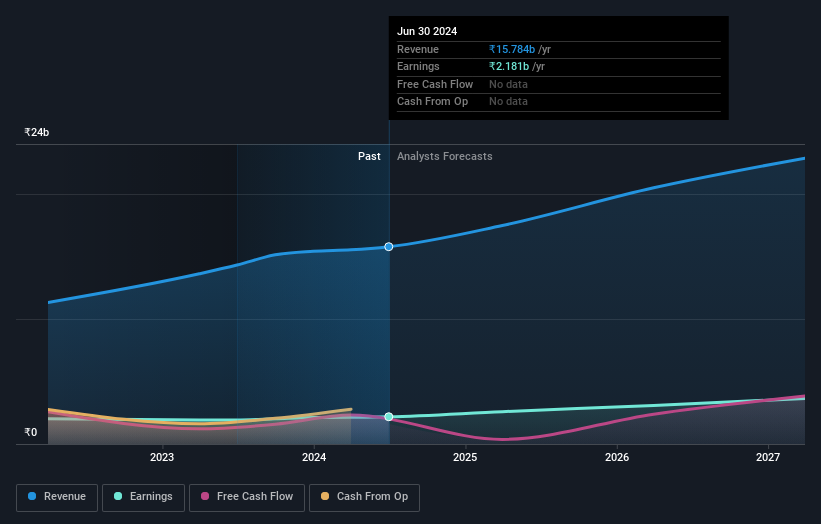

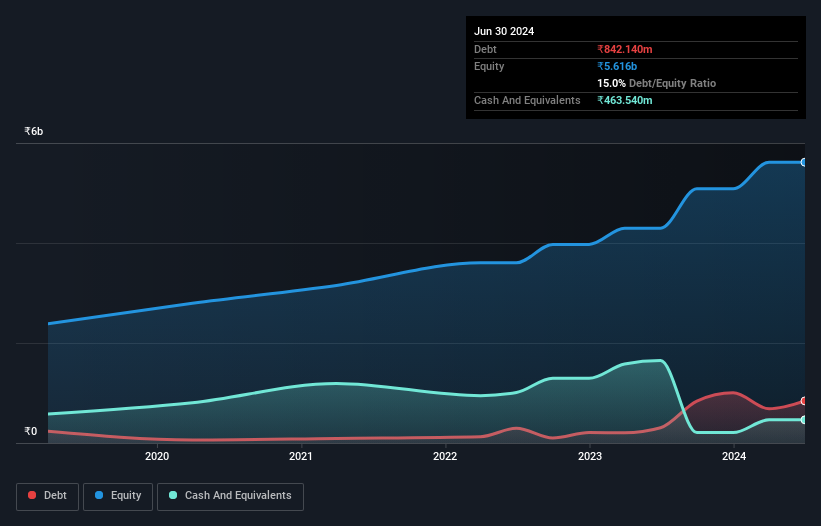

Vindhya Telelinks (NSEI:VINDHYATEL)

Simply Wall St Value Rating: ★★★★★★

Overview: Vindhya Telelinks Limited is an Indian company specializing in the manufacture and sale of cables, with a market capitalization of ₹31.44 billion.

Operations: The company generates its revenue primarily from two segments: Cable, which brought in ₹5.94 billion, and Engineering, Procurement & Construction (EPC), which accounted for ₹35.24 billion. It has observed a gross profit margin of 14.74% as of the latest reporting period in 2024.

Vindhya Telelinks, trading at 77% below its estimated fair value, presents a compelling case as an overlooked gem. Despite not outperforming the Communications industry with a year-over-year earnings growth of 52.5%, it has reduced its debt-to-equity ratio significantly from 34.7% to 12% over five years. The company's net debt to equity stands at a satisfactory 8.2%. Recent financials show robust annual revenue growth to INR 41,101 million and net income increase to INR 2,827 million for FY2024, up from INR 29,139 million and INR 1,853 million respectively in the previous year.

Vindhya Telelinks (NSEI:VINDHYATEL)

Simply Wall St Value Rating: ★★★★★★

Overview: Vindhya Telelinks Limited is an Indian company specializing in the manufacture and sale of cables, with a market capitalization of ₹31.44 billion.

Operations: The company generates its revenue primarily from two segments: Cable, which brought in ₹5.94 billion, and Engineering, Procurement & Construction (EPC), which accounted for ₹35.24 billion. It has observed a gross profit margin of 14.74% as of the latest reporting period in 2024.

Vindhya Telelinks, trading at 77% below its estimated fair value, presents a compelling case as an overlooked gem. Despite not outperforming the Communications industry with a year-over-year earnings growth of 52.5%, it has reduced its debt-to-equity ratio significantly from 34.7% to 12% over five years. The company's net debt to equity stands at a satisfactory 8.2%. Recent financials show robust annual revenue growth to INR 41,101 million and net income increase to INR 2,827 million for FY2024, up from INR 29,139 million and INR 1,853 million respectively in the previous year.

Turning Ideas Into Actions

- Embark on your investment journey to our 458 Indian Undiscovered Gems With Strong Fundamentals selection here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:VINDHYATEL

Vindhya Telelinks

Engages in the manufacture and sale of cables in India.

Solid track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor