When VIP Clothing Limited (NSE:VIPCLOTHNG) reported its results to June 2021 its auditors, Sharp & Tannan could not be sure that it would be able to continue as a going concern in the next year. Thus we can say that, based on the results to that date, the company should raise capital or otherwise raise cash, without much delay.

Since the company probably needs cash fairly quickly, it may be in a position where it has to accept whatever terms it can get. So shareholders should absolutely be taking a close look at how risky the balance sheet is. Debt is always a risk factor in these cases, as creditors could be in a position to wind up the company, in the worst case scenario.

Check out our latest analysis for VIP Clothing

What Is VIP Clothing's Debt?

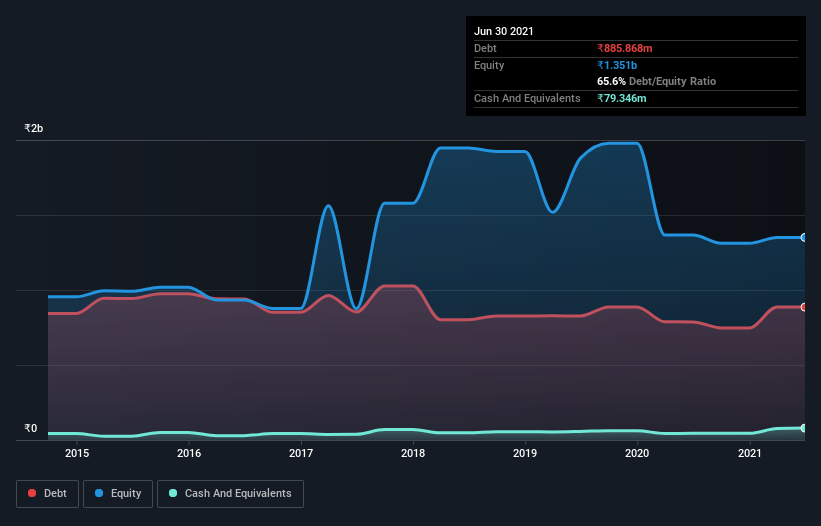

As you can see below, at the end of March 2021, VIP Clothing had ₹885.9m of debt, up from ₹787.3m a year ago. Click the image for more detail. However, it does have ₹79.3m in cash offsetting this, leading to net debt of about ₹806.5m.

How Healthy Is VIP Clothing's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that VIP Clothing had liabilities of ₹1.13b due within 12 months and liabilities of ₹224.9m due beyond that. Offsetting these obligations, it had cash of ₹79.3m as well as receivables valued at ₹754.9m due within 12 months. So it has liabilities totalling ₹516.7m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since VIP Clothing has a market capitalization of ₹1.54b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

VIP Clothing shareholders face the double whammy of a high net debt to EBITDA ratio (15.9), and fairly weak interest coverage, since EBIT is just 0.085 times the interest expense. The debt burden here is substantial. However, the silver lining was that VIP Clothing achieved a positive EBIT of ₹8.8m in the last twelve months, an improvement on the prior year's loss. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since VIP Clothing will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Happily for any shareholders, VIP Clothing actually produced more free cash flow than EBIT over the last year. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Neither VIP Clothing's ability to cover its interest expense with its EBIT nor its net debt to EBITDA gave us confidence in its ability to take on more debt. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that VIP Clothing is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. While some investors may specialize in these sort of situations, it's simply too risky and complicated for us to want to invest in a company after an auditor has expressed doubts about its ability to continue as a going concern. We prefer to invest in companies that ensure the balance sheet remains healthier than that. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should learn about the 3 warning signs we've spotted with VIP Clothing (including 1 which shouldn't be ignored) .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade VIP Clothing, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:VIPCLOTHNG

VIP Clothing

Engages in the manufacture, marketing, and distribution of garments in India.

Excellent balance sheet very low.

Similar Companies

Market Insights

Community Narratives