Advertisement

If EPS Growth Is Important To You, United Polyfab Gujarat (NSE:UNITEDPOLY) Presents An Opportunity

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in United Polyfab Gujarat (NSE:UNITEDPOLY). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

United Polyfab Gujarat's Earnings Per Share Are Growing

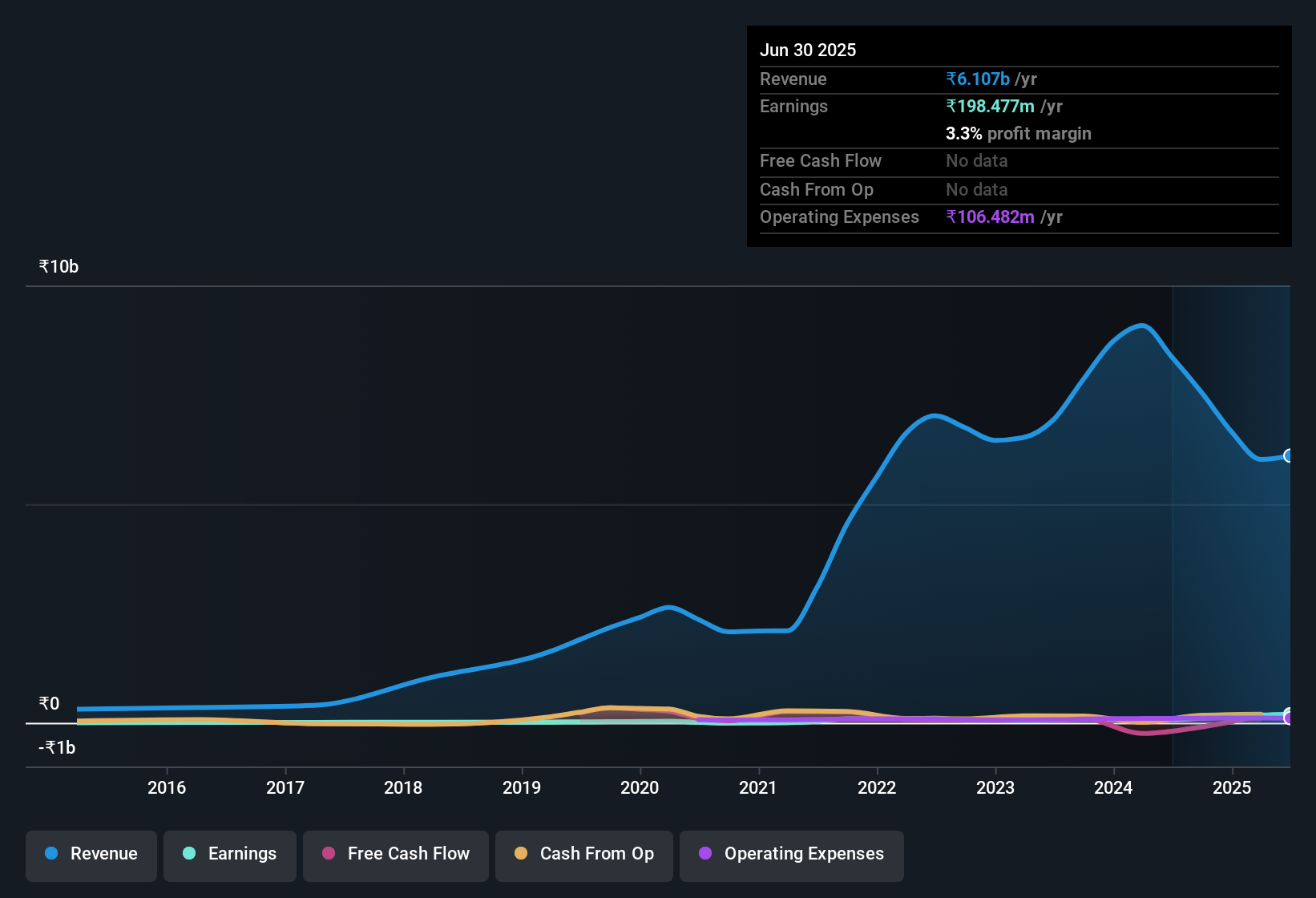

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. That makes EPS growth an attractive quality for any company. It certainly is nice to see that United Polyfab Gujarat has managed to grow EPS by 20% per year over three years. So it's not surprising to see the company trades on a very high multiple of (past) earnings.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. United Polyfab Gujarat's EBIT margins have actually improved by 3.4 percentage points in the last year, to reach 5.7%, but, on the flip side, revenue was down 27%. That falls short of ideal.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

See our latest analysis for United Polyfab Gujarat

Since United Polyfab Gujarat is no giant, with a market capitalisation of ₹10b, you should definitely check its cash and debt before getting too excited about its prospects.

Are United Polyfab Gujarat Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

The first bit of good news is that no United Polyfab Gujarat insiders reported share sales in the last twelve months. Even better, though, is that the Chairman of the Board & MD, Gagan Mittal, bought a whopping ₹40m worth of shares, paying about ₹14.30 per share, on average. It seems at least one insider thinks that the company is doing well - and they are backing that view with cash.

On top of the insider buying, we can also see that United Polyfab Gujarat insiders own a large chunk of the company. In fact, they own 41% of the shares, making insiders a very influential shareholder group. This should be a welcoming sign for investors because it suggests that the people making the decisions are also impacted by their choices. In terms of absolute value, insiders have ₹4.2b invested in the business, at the current share price. So there's plenty there to keep them focused!

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. That's because on our analysis the CEO, Gagan Mittal, is paid less than the median for similar sized companies. The median total compensation for CEOs of companies similar in size to United Polyfab Gujarat, with market caps under ₹18b is around ₹4.1m.

The CEO of United Polyfab Gujarat was paid just ₹1.8m in total compensation for the year ending March 2025. This total may indicate that the CEO is sacrificing take home pay for performance-based benefits, ensuring that their motivations are synonymous with strong company results. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Should You Add United Polyfab Gujarat To Your Watchlist?

For growth investors, United Polyfab Gujarat's raw rate of earnings growth is a beacon in the night. On top of that, insiders own a significant piece of the pie when it comes to the company's stock, and one has been buying more. Astute investors will want to keep this stock on watch. We should say that we've discovered 2 warning signs for United Polyfab Gujarat (1 can't be ignored!) that you should be aware of before investing here.

The good news is that United Polyfab Gujarat is not the only stock with insider buying. Here's a list of small cap, undervalued companies in IN with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:UNITEDPOLY

United Polyfab Gujarat

Manufactures, trades in, and sells woven fabrics and processed yarn products in India.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor