Advertisement

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For Superhouse Limited's (NSE:SUPERHOUSE) CEO For Now

Key Insights

- Superhouse to hold its Annual General Meeting on 30th of September

- CEO Mukhtarul Amin's total compensation includes salary of ₹12.0m

- The total compensation is 277% higher than the average for the industry

- Over the past three years, Superhouse's EPS grew by 5.7% and over the past three years, the total shareholder return was 164%

CEO Mukhtarul Amin has done a decent job of delivering relatively good performance at Superhouse Limited (NSE:SUPERHOUSE) recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 30th of September. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

View our latest analysis for Superhouse

How Does Total Compensation For Mukhtarul Amin Compare With Other Companies In The Industry?

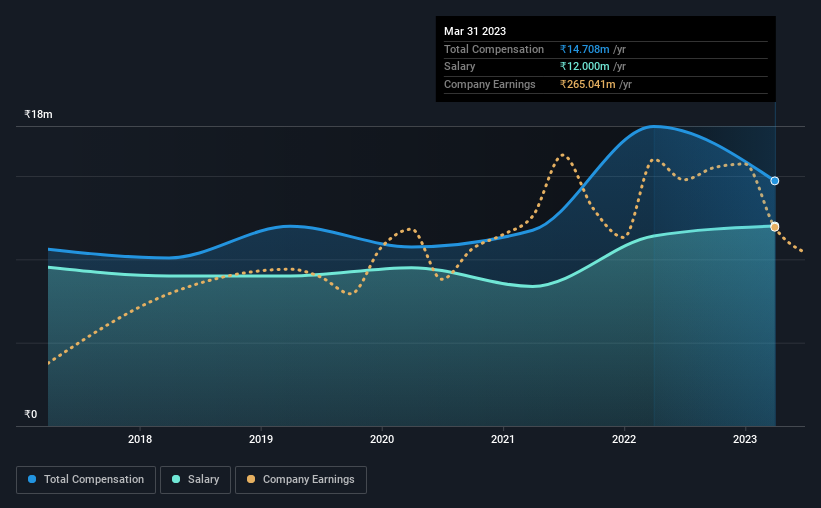

According to our data, Superhouse Limited has a market capitalization of ₹2.4b, and paid its CEO total annual compensation worth ₹15m over the year to March 2023. We note that's a decrease of 18% compared to last year. In particular, the salary of ₹12.0m, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the Indian Luxury industry with market capitalizations below ₹17b, reported a median total CEO compensation of ₹3.9m. Hence, we can conclude that Mukhtarul Amin is remunerated higher than the industry median. What's more, Mukhtarul Amin holds ₹284m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | ₹12m | ₹11m | 82% |

| Other | ₹2.7m | ₹6.6m | 18% |

| Total Compensation | ₹15m | ₹18m | 100% |

Speaking on an industry level, all of total compensation represents salary, while non-salary remuneration is completely ignored. It's interesting to note that Superhouse allocates a smaller portion of compensation to salary in comparison to the broader industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Superhouse Limited's Growth

Superhouse Limited's earnings per share (EPS) grew 5.7% per year over the last three years. It achieved revenue growth of 10% over the last year.

We would argue that the modest growth in revenue is a notable positive. And the improvement in EPSis modest but respectable. Although we'll stop short of calling the stock a top performer, we think the company has potential. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Superhouse Limited Been A Good Investment?

We think that the total shareholder return of 164%, over three years, would leave most Superhouse Limited shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 3 warning signs for Superhouse that you should be aware of before investing.

Switching gears from Superhouse, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SUPERHOUSE

Superhouse

Engages in the manufacture and sale of leather and leather products, as well as textile garments in India and internationally.

Moderate risk with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor