Shareholders Will Probably Hold Off On Increasing Superhouse Limited's (NSE:SUPERHOUSE) CEO Compensation For The Time Being

Performance at Superhouse Limited (NSE:SUPERHOUSE) has been reasonably good and CEO Mukhtarul Amin has done a decent job of steering the company in the right direction. As shareholders go into the upcoming AGM on 30 September 2022, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still want to keep CEO compensation within reason.

Check out our latest analysis for Superhouse

Comparing Superhouse Limited's CEO Compensation With The Industry

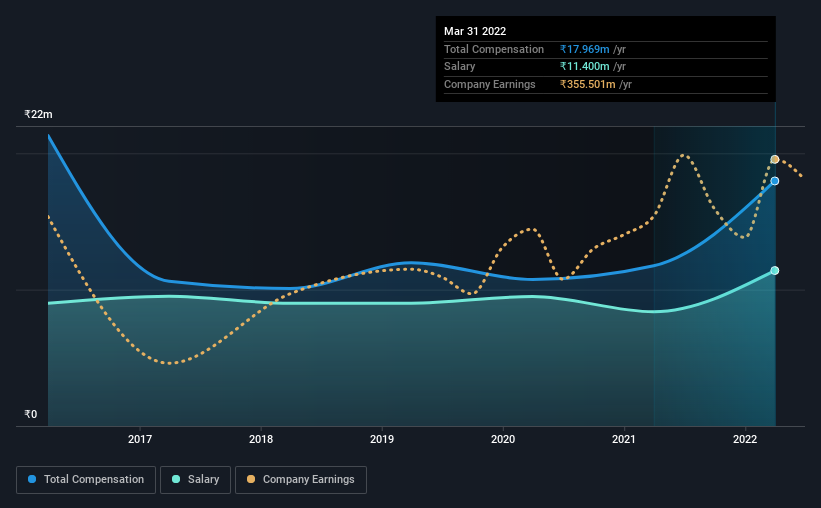

At the time of writing, our data shows that Superhouse Limited has a market capitalization of ₹2.4b, and reported total annual CEO compensation of ₹18m for the year to March 2022. We note that's an increase of 53% above last year. We note that the salary portion, which stands at ₹11.4m constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the industry with market capitalizations below ₹16b, we found that the median total CEO compensation was ₹3.6m. This suggests that Mukhtarul Amin is paid more than the median for the industry. What's more, Mukhtarul Amin holds ₹284m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | ₹11m | ₹8.4m | 63% |

| Other | ₹6.6m | ₹3.4m | 37% |

| Total Compensation | ₹18m | ₹12m | 100% |

Talking in terms of the industry, salary represented approximately 100% of total compensation out of all the companies we analyzed, while other remuneration made up 0.0015% of the pie. It's interesting to note that Superhouse allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Superhouse Limited's Growth

Over the past three years, Superhouse Limited has seen its earnings per share (EPS) grow by 18% per year. In the last year, its revenue is up 13%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Superhouse Limited Been A Good Investment?

We think that the total shareholder return of 163%, over three years, would leave most Superhouse Limited shareholders smiling. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 3 warning signs for Superhouse (1 can't be ignored!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SUPERHOUSE

Superhouse

Engages in the manufacture and sale of leather and leather products, as well as textile garments in India and internationally.

Adequate balance sheet with slight risk.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion