Indo Count Industries Limited's (NSE:ICIL) Fundamentals Look Pretty Strong: Could The Market Be Wrong About The Stock?

With its stock down 17% over the past month, it is easy to disregard Indo Count Industries (NSE:ICIL). However, stock prices are usually driven by a company’s financial performance over the long term, which in this case looks quite promising. In this article, we decided to focus on Indo Count Industries' ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for Indo Count Industries

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Indo Count Industries is:

14% = ₹3.1b ÷ ₹22b (Based on the trailing twelve months to September 2024).

The 'return' is the yearly profit. So, this means that for every ₹1 of its shareholder's investments, the company generates a profit of ₹0.14.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Indo Count Industries' Earnings Growth And 14% ROE

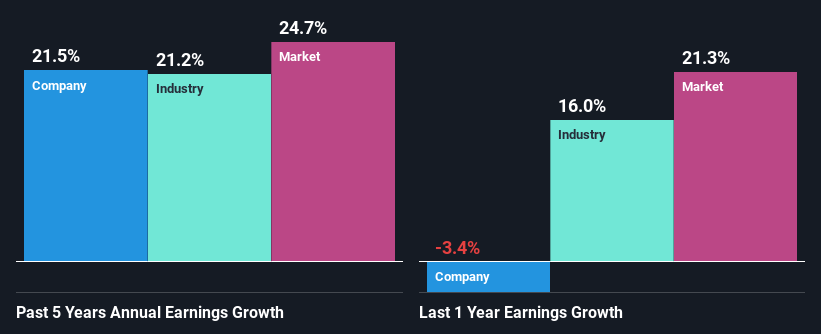

On the face of it, Indo Count Industries' ROE is not much to talk about. Although a closer study shows that the company's ROE is higher than the industry average of 8.3% which we definitely can't overlook. Especially when you consider Indo Count Industries' exceptional 22% net income growth over the past five years. That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. Therefore, the growth in earnings could also be the result of other factors. For example, it is possible that the broader industry is going through a high growth phase, or that the company has a low payout ratio.

We then performed a comparison between Indo Count Industries' net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 21% in the same 5-year period.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. Is Indo Count Industries fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Indo Count Industries Making Efficient Use Of Its Profits?

Indo Count Industries' three-year median payout ratio to shareholders is 13%, which is quite low. This implies that the company is retaining 87% of its profits. This suggests that the management is reinvesting most of the profits to grow the business as evidenced by the growth seen by the company.

Moreover, Indo Count Industries is determined to keep sharing its profits with shareholders which we infer from its long history of nine years of paying a dividend. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 17% over the next three years. Regardless, the future ROE for Indo Count Industries is speculated to rise to 17% despite the anticipated increase in the payout ratio. There could probably be other factors that could be driving the future growth in the ROE.

Conclusion

Overall, we are quite pleased with Indo Count Industries' performance. Specifically, we like that it has been reinvesting a high portion of its profits at a moderate rate of return, resulting in earnings expansion. The latest industry analyst forecasts show that the company is expected to maintain its current growth rate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ICIL

Indo Count Industries

Manufactures and sells home textile products in India and internationally.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion