Advertisement

Banaras Beads Limited (NSE:BANARBEADS) Is Going Strong But Fundamentals Appear To Be Mixed : Is There A Clear Direction For The Stock?

Banaras Beads' (NSE:BANARBEADS) stock is up by a considerable 17% over the past month. However, we wonder if the company's inconsistent financials would have any adverse impact on the current share price momentum. Specifically, we decided to study Banaras Beads' ROE in this article.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

See our latest analysis for Banaras Beads

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Banaras Beads is:

5.2% = ₹28m ÷ ₹542m (Based on the trailing twelve months to June 2024).

The 'return' is the yearly profit. Another way to think of that is that for every ₹1 worth of equity, the company was able to earn ₹0.05 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Banaras Beads' Earnings Growth And 5.2% ROE

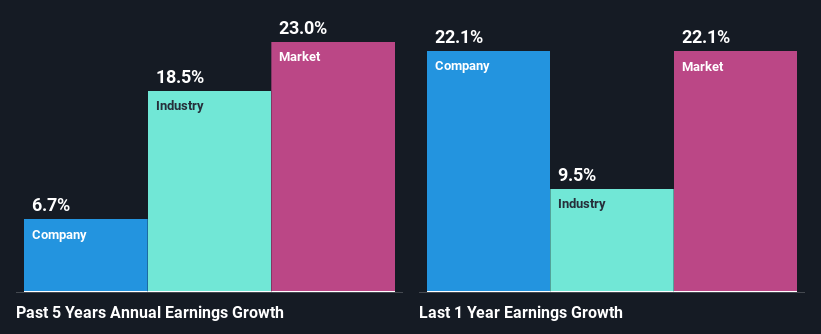

As you can see, Banaras Beads' ROE looks pretty weak. Not just that, even compared to the industry average of 7.8%, the company's ROE is entirely unremarkable. Although, we can see that Banaras Beads saw a modest net income growth of 6.7% over the past five years. We believe that there might be other aspects that are positively influencing the company's earnings growth. For instance, the company has a low payout ratio or is being managed efficiently.

As a next step, we compared Banaras Beads' net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 18% in the same period.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is Banaras Beads fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Banaras Beads Making Efficient Use Of Its Profits?

While Banaras Beads has a three-year median payout ratio of 51% (which means it retains 49% of profits), the company has still seen a fair bit of earnings growth in the past, meaning that its high payout ratio hasn't hampered its ability to grow.

Besides, Banaras Beads has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders.

Summary

On the whole, we feel that the performance shown by Banaras Beads can be open to many interpretations. While no doubt its earnings growth is pretty respectable, the low profit retention could mean that the company's earnings growth could have been higher, had it been paying reinvesting a higher portion of its profits. An improvement in its ROE could also help future earnings growth. So far, we've only made a quick discussion around the company's earnings growth. You can do your own research on Banaras Beads and see how it has performed in the past by looking at this FREE detailed graph of past earnings, revenue and cash flows.

Valuation is complex, but we're here to simplify it.

Discover if Banaras Beads might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BANARBEADS

Banaras Beads

Engages in the manufacture and sale of glass beads, necklaces, jewelries, and accessories under the De-Lemon brand in India, the United States, South Africa, the United Kingdom, Ireland, Germany, Europe, the Middle East, and Africa.

Excellent balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor