Advertisement

- India

- /

- Consumer Durables

- /

- NSEI:AMBER

These 4 Measures Indicate That Amber Enterprises India (NSE:AMBER) Is Using Debt Extensively

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Amber Enterprises India Limited (NSE:AMBER) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Amber Enterprises India

How Much Debt Does Amber Enterprises India Carry?

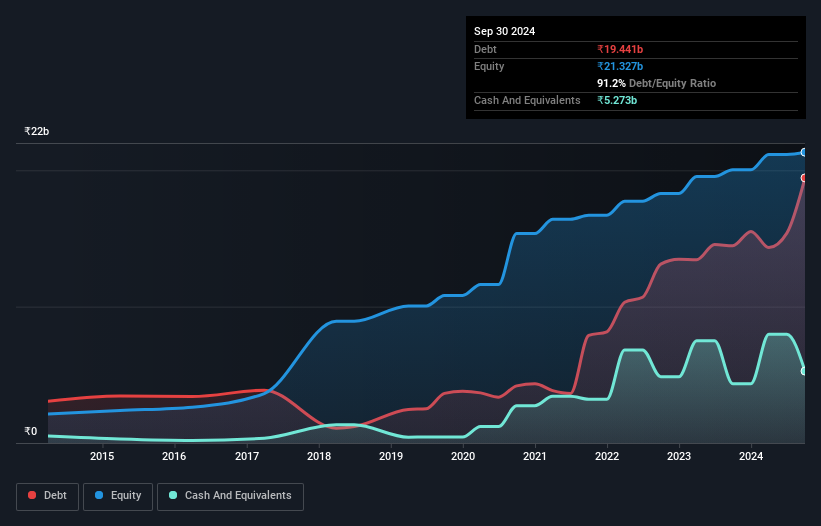

As you can see below, at the end of September 2024, Amber Enterprises India had ₹19.4b of debt, up from ₹14.5b a year ago. Click the image for more detail. However, it also had ₹5.27b in cash, and so its net debt is ₹14.2b.

How Strong Is Amber Enterprises India's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Amber Enterprises India had liabilities of ₹29.9b due within 12 months and liabilities of ₹13.0b due beyond that. Offsetting these obligations, it had cash of ₹5.27b as well as receivables valued at ₹12.5b due within 12 months. So its liabilities total ₹25.2b more than the combination of its cash and short-term receivables.

Given Amber Enterprises India has a market capitalization of ₹206.8b, it's hard to believe these liabilities pose much threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Amber Enterprises India's debt is 2.5 times its EBITDA, and its EBIT cover its interest expense 2.8 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. One way Amber Enterprises India could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 18%, as it did over the last year. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Amber Enterprises India can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Considering the last three years, Amber Enterprises India actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Both Amber Enterprises India's conversion of EBIT to free cash flow and its interest cover were discouraging. But on the brighter side of life, its EBIT growth rate leaves us feeling more frolicsome. Looking at all the angles mentioned above, it does seem to us that Amber Enterprises India is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Amber Enterprises India , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:AMBER

Amber Enterprises India

Provides room air conditioner solutions in India.

Solid track record with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor