Advertisement

- India

- /

- Professional Services

- /

- NSEI:TEAMLEASE

The Price Is Right For TeamLease Services Limited (NSE:TEAMLEASE) Even After Diving 26%

The TeamLease Services Limited (NSE:TEAMLEASE) share price has fared very poorly over the last month, falling by a substantial 26%. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 37% in that time.

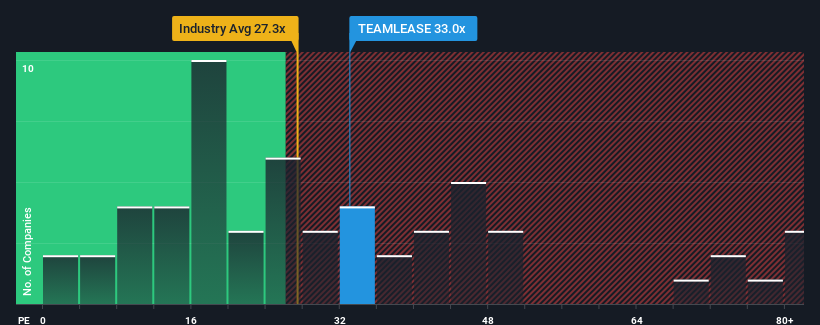

Even after such a large drop in price, TeamLease Services may still be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 33x, since almost half of all companies in India have P/E ratios under 26x and even P/E's lower than 15x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

While the market has experienced earnings growth lately, TeamLease Services' earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

View our latest analysis for TeamLease Services

Does Growth Match The High P/E?

In order to justify its P/E ratio, TeamLease Services would need to produce impressive growth in excess of the market.

Retrospectively, the last year delivered a frustrating 6.0% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 290% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 39% per year during the coming three years according to the twelve analysts following the company. With the market only predicted to deliver 18% each year, the company is positioned for a stronger earnings result.

In light of this, it's understandable that TeamLease Services' P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From TeamLease Services' P/E?

Despite the recent share price weakness, TeamLease Services' P/E remains higher than most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that TeamLease Services maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

The company's balance sheet is another key area for risk analysis. You can assess many of the main risks through our free balance sheet analysis for TeamLease Services with six simple checks.

If you're unsure about the strength of TeamLease Services' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if TeamLease Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TEAMLEASE

TeamLease Services

Engages in human resource services in India and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor