Advertisement

- India

- /

- Commercial Services

- /

- NSEI:IRCTC

Some Confidence Is Lacking In Indian Railway Catering & Tourism Corporation Limited's (NSE:IRCTC) P/E

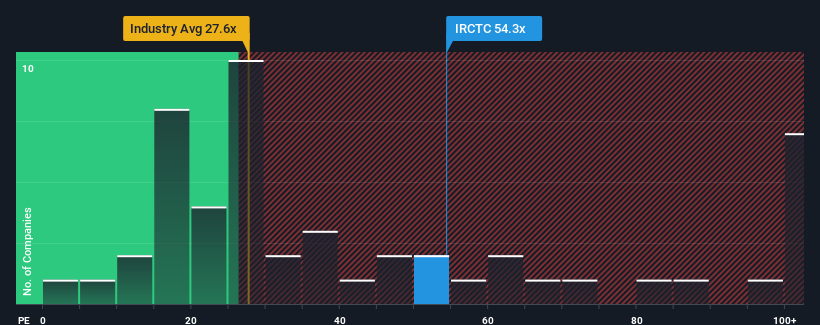

Indian Railway Catering & Tourism Corporation Limited's (NSE:IRCTC) price-to-earnings (or "P/E") ratio of 54.3x might make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 31x and even P/E's below 18x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

With earnings growth that's inferior to most other companies of late, Indian Railway Catering & Tourism has been relatively sluggish. One possibility is that the P/E is high because investors think this lacklustre earnings performance will improve markedly. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Indian Railway Catering & Tourism

Is There Enough Growth For Indian Railway Catering & Tourism?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Indian Railway Catering & Tourism's to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 13% last year. Pleasingly, EPS has also lifted 184% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 16% each year as estimated by the eight analysts watching the company. With the market predicted to deliver 19% growth per year, the company is positioned for a weaker earnings result.

In light of this, it's alarming that Indian Railway Catering & Tourism's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

What We Can Learn From Indian Railway Catering & Tourism's P/E?

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Indian Railway Catering & Tourism's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Indian Railway Catering & Tourism (1 is significant!) that you need to be mindful of.

You might be able to find a better investment than Indian Railway Catering & Tourism. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:IRCTC

Indian Railway Catering & Tourism

Engages in the provision of catering and hospitality, Internet ticketing, travel and tourism, and packaged drinking water services in India.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

63 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PicaCoder on Microsoft ·

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value:US$42015.0% overvalued

60 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

63 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative