Advertisement

- India

- /

- Hospitality

- /

- NSEI:APOLSINHOT

How Does Apollo Sindoori Hotels Limited's (NSE:APOLSINHOT) Earnings Growth Stack Up Against The Industry?

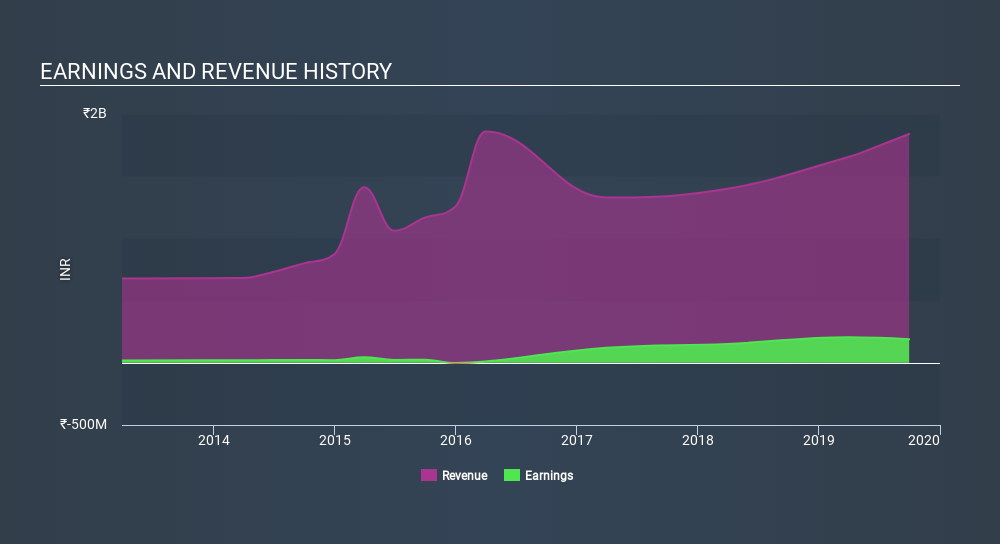

Assessing Apollo Sindoori Hotels Limited's (NSEI:APOLSINHOT) past track record of performance is a useful exercise for investors. It allows us to understand whether the company has met or exceed expectations, which is a great indicator for future performance. Below, I assess APOLSINHOT's latest performance announced on 30 September 2019 and evaluate these figures to its historical trend and industry movements.

Check out our latest analysis for Apollo Sindoori Hotels

Did APOLSINHOT beat its long-term earnings growth trend and its industry?

APOLSINHOT's trailing twelve-month earnings (from 30 September 2019) of ₹190m has increased by 6.0% compared to the previous year.

However, this one-year growth rate has been lower than its average earnings growth rate over the past 5 years of 50%, indicating the rate at which APOLSINHOT is growing has slowed down. To understand what's happening, let's examine what's going on with margins and if the rest of the industry is facing the same headwind.

In terms of returns from investment, Apollo Sindoori Hotels has invested its equity funds well leading to a 25% return on equity (ROE), above the sensible minimum of 20%. Furthermore, its return on assets (ROA) of 16% exceeds the IN Commercial Services industry of 7.2%, indicating Apollo Sindoori Hotels has used its assets more efficiently. However, its return on capital (ROC), which also accounts for Apollo Sindoori Hotels’s debt level, has declined over the past 3 years from 26% to 13%. This correlates with an increase in debt holding, with debt-to-equity ratio rising from 4.9% to 7.8% over the past 5 years.

What does this mean?

While past data is useful, it doesn’t tell the whole story. Positive growth and profitability are what investors like to see in a company’s track record, but how do we properly assess sustainability? You should continue to research Apollo Sindoori Hotels to get a better picture of the stock by looking at:

- Financial Health: Are APOLSINHOT’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

- Valuation: What is APOLSINHOT worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether APOLSINHOT is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 30 September 2019. This may not be consistent with full year annual report figures.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NSEI:APOLSINHOT

Apollo Sindoori Hotels

Operates as a hospitality service management and support services company in India.

Excellent balance sheet low.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor