Advertisement

W.S. Industries (India) Limited (NSE:WSI) Stock Rockets 41% But Many Are Still Ignoring The Company

W.S. Industries (India) Limited (NSE:WSI) shareholders have had their patience rewarded with a 41% share price jump in the last month. The last 30 days were the cherry on top of the stock's 964% gain in the last year, which is nothing short of spectacular.

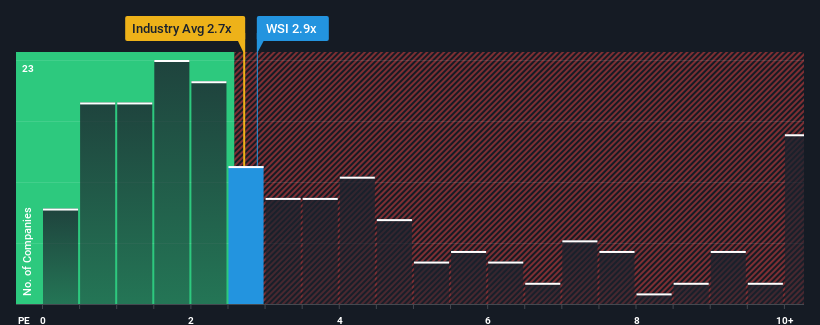

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about W.S. Industries (India)'s P/S ratio of 2.9x, since the median price-to-sales (or "P/S") ratio for the Machinery industry in India is also close to 2.7x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for W.S. Industries (India)

What Does W.S. Industries (India)'s Recent Performance Look Like?

With revenue growth that's exceedingly strong of late, W.S. Industries (India) has been doing very well. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. Those who are bullish on W.S. Industries (India) will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for W.S. Industries (India), take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The P/S?

The only time you'd be comfortable seeing a P/S like W.S. Industries (India)'s is when the company's growth is tracking the industry closely.

Taking a look back first, we see that the company's revenues underwent some rampant growth over the last 12 months. Spectacularly, three year revenue growth has also set the world alight, thanks to the last 12 months of incredible growth. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

When compared to the industry's one-year growth forecast of 12%, the most recent medium-term revenue trajectory is noticeably more alluring

In light of this, it's curious that W.S. Industries (India)'s P/S sits in line with the majority of other companies. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Final Word

Its shares have lifted substantially and now W.S. Industries (India)'s P/S is back within range of the industry median. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

To our surprise, W.S. Industries (India) revealed its three-year revenue trends aren't contributing to its P/S as much as we would have predicted, given they look better than current industry expectations. It'd be fair to assume that potential risks the company faces could be the contributing factor to the lower than expected P/S. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with W.S. Industries (India) (at least 2 which can't be ignored), and understanding these should be part of your investment process.

If these risks are making you reconsider your opinion on W.S. Industries (India), explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if W.S. Industries (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:WSI

W.S. Industries (India)

Engages in the manufacture and sale of porcelain insulators for electrical high voltage transmission, substation, and distribution applications in India and internationally.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor