Advertisement

Technocraft Industries (India) (NSE:TIIL) Looks To Prolong Its Impressive Returns

What trends should we look for it we want to identify stocks that can multiply in value over the long term? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. That's why when we briefly looked at Technocraft Industries (India)'s (NSE:TIIL) ROCE trend, we were very happy with what we saw.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Technocraft Industries (India), this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.20 = ₹3.5b ÷ (₹26b - ₹8.4b) (Based on the trailing twelve months to December 2023).

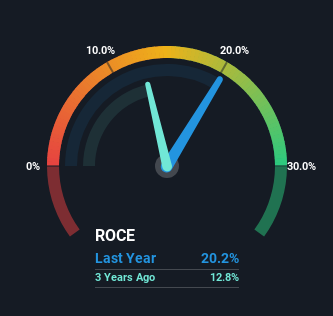

Therefore, Technocraft Industries (India) has an ROCE of 20%. In absolute terms that's a very respectable return and compared to the Machinery industry average of 18% it's pretty much on par.

See our latest analysis for Technocraft Industries (India)

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Technocraft Industries (India), check out these free graphs here.

How Are Returns Trending?

It's hard not to be impressed by Technocraft Industries (India)'s returns on capital. Over the past five years, ROCE has remained relatively flat at around 20% and the business has deployed 104% more capital into its operations. Returns like this are the envy of most businesses and given it has repeatedly reinvested at these rates, that's even better. If these trends can continue, it wouldn't surprise us if the company became a multi-bagger.

One more thing to note, even though ROCE has remained relatively flat over the last five years, the reduction in current liabilities to 33% of total assets, is good to see from a business owner's perspective. This can eliminate some of the risks inherent in the operations because the business has less outstanding obligations to their suppliers and or short-term creditors than they did previously.

What We Can Learn From Technocraft Industries (India)'s ROCE

In short, we'd argue Technocraft Industries (India) has the makings of a multi-bagger since its been able to compound its capital at very profitable rates of return. And long term investors would be thrilled with the 314% return they've received over the last five years. So while investors seem to be recognizing these promising trends, we still believe the stock deserves further research.

Before jumping to any conclusions though, we need to know what value we're getting for the current share price. That's where you can check out our FREE intrinsic value estimation that compares the share price and estimated value.

Technocraft Industries (India) is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

Valuation is complex, but we're here to simplify it.

Discover if Technocraft Industries (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TIIL

Technocraft Industries (India)

Engages in scaffolding business in India and internationally.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor