Advertisement

Over the last 7 days, the Indian market has dropped 1.7%, driven by a loss of 2.3% in the Financials sector, although it has risen by 43% in the last year. In this fluctuating environment, identifying growth companies with high insider ownership can be crucial as they often indicate strong confidence from those who know the business best and are positioned to benefit from expected earnings growth of 17% per annum over the next few years.

Top 10 Growth Companies With High Insider Ownership In India

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 35% |

| Kirloskar Pneumatic (BSE:505283) | 30.6% | 30.1% |

| Dixon Technologies (India) (NSEI:DIXON) | 24.6% | 35.7% |

| Jupiter Wagons (NSEI:JWL) | 10.8% | 27.2% |

| Happiest Minds Technologies (NSEI:HAPPSTMNDS) | 31.9% | 20.7% |

| Paisalo Digital (BSE:532900) | 16.3% | 24.8% |

| JNK India (NSEI:JNKINDIA) | 21% | 31.8% |

| KEI Industries (BSE:517569) | 19.1% | 20.3% |

| Apollo Hospitals Enterprise (NSEI:APOLLOHOSP) | 10.4% | 33% |

| Aether Industries (NSEI:AETHER) | 31.1% | 43.6% |

Let's explore several standout options from the results in the screener.

Sansera Engineering (NSEI:SANSERA)

Simply Wall St Growth Rating: ★★★★★☆

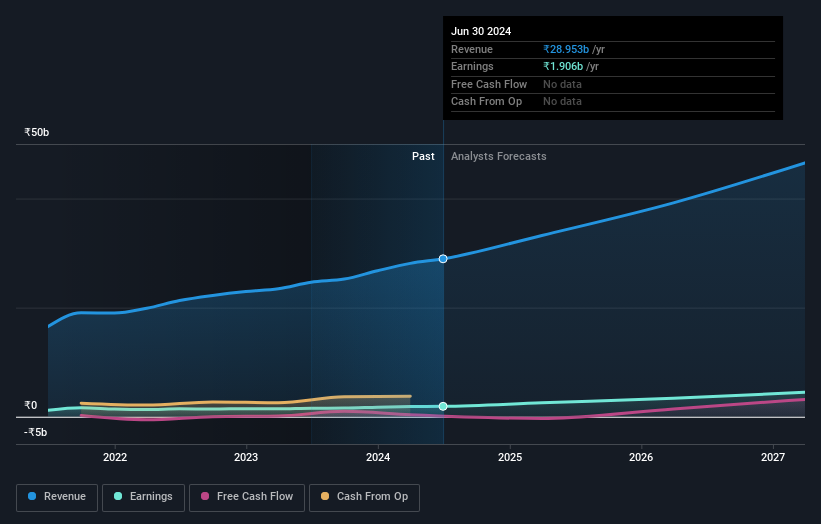

Overview: Sansera Engineering Limited manufactures and sells high precision components for automotive and non-automotive sectors across India, Europe, the United States, and internationally, with a market cap of ₹75.27 billion.

Operations: The company generates revenue of ₹28.95 billion from the manufacture of precision-engineered components.

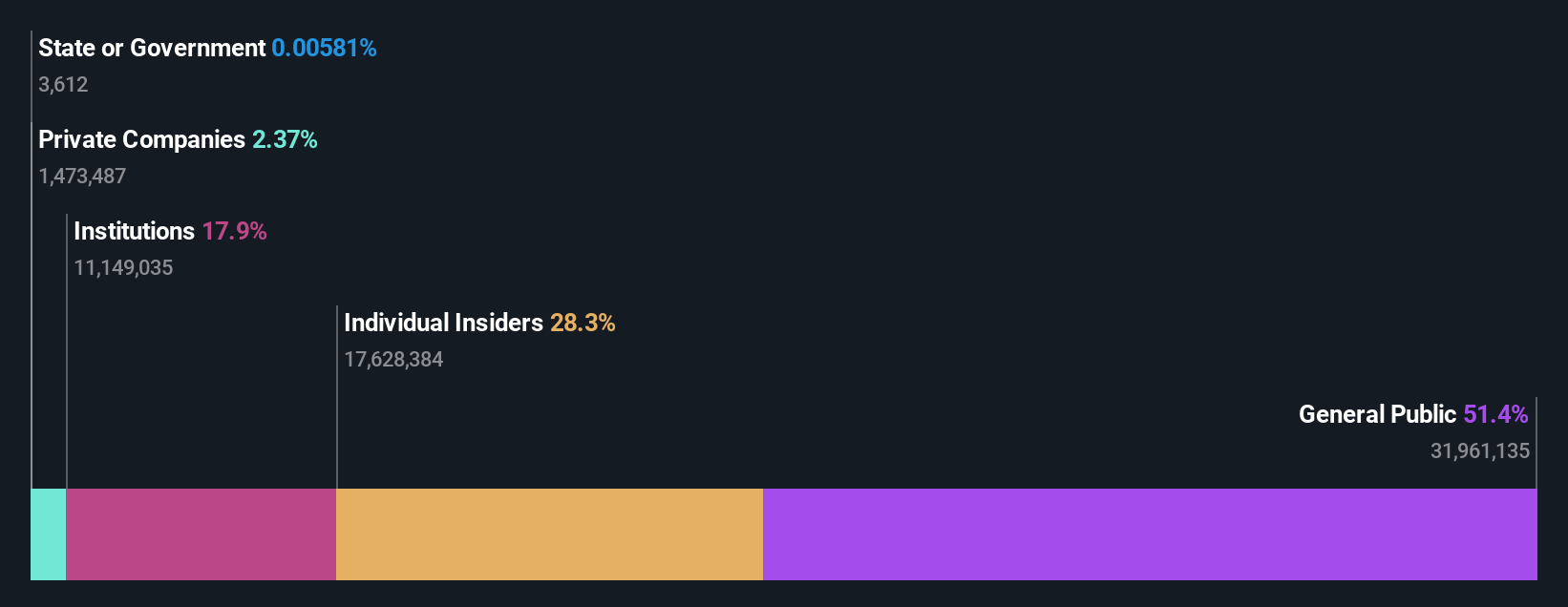

Insider Ownership: 34.9%

Revenue Growth Forecast: 15.3% p.a.

Sansera Engineering, with significant insider ownership, is forecasted to see earnings grow 28.78% annually, outpacing the Indian market's 16.9%. Recent Q1 results show a revenue increase to ₹7.44 billion and net income of ₹495.77 million. The company plans a major expansion in Karnataka, investing ₹21 billion over 3-5 years to boost manufacturing capacity and create jobs. Despite high debt levels, Sansera's strategic growth initiatives highlight its potential as a robust growth company in India.

- Get an in-depth perspective on Sansera Engineering's performance by reading our analyst estimates report here.

- The analysis detailed in our Sansera Engineering valuation report hints at an inflated share price compared to its estimated value.

Tega Industries (NSEI:TEGA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Tega Industries Limited designs, manufactures, and installs process equipment and accessories for the mineral processing, mining, and material handling industries with a market cap of ₹118.67 billion.

Operations: Tega Industries generates revenue from the design, manufacture, and installation of equipment and accessories for mineral processing, mining, and material handling industries.

Insider Ownership: 19%

Revenue Growth Forecast: 17% p.a.

Tega Industries, with substantial insider ownership, is expected to see earnings grow 24.75% annually, surpassing the Indian market's 16.9%. Recent Q1 results show a revenue increase to ₹3.52 billion and net income of ₹367.44 million. Despite slower revenue growth forecasts (17% per year), the company's high return on equity (21.6%) in three years and strong historical earnings growth underscore its potential as a significant growth company in India.

- Unlock comprehensive insights into our analysis of Tega Industries stock in this growth report.

- According our valuation report, there's an indication that Tega Industries' share price might be on the expensive side.

VA Tech Wabag (NSEI:WABAG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: VA Tech Wabag Limited, with a market cap of ₹78.36 billion, specializes in the design, supply, installation, construction, operation, and maintenance of drinking water, waste and industrial water treatment, and desalination plants both in India and internationally.

Operations: The company's revenue segments include ₹7.14 billion from drinking water treatment, ₹5.62 billion from waste water treatment, ₹3.48 billion from industrial water treatment, and ₹2.36 billion from desalination plants.

Insider Ownership: 29.5%

Revenue Growth Forecast: 15.2% p.a.

VA Tech Wabag, with significant insider ownership, is forecast to grow earnings by 22.8% annually, outpacing the Indian market's 16.9%. Recent Q1 results show revenue rising to ₹6.37 billion and net income at ₹550 million. Despite a moderate price-to-earnings ratio of 31.3x compared to the market's 33.8x, insiders have shown limited buying activity recently. The company's revenue growth rate (15.2% per year) is expected to be above the market average but below high-growth thresholds.

- Click to explore a detailed breakdown of our findings in VA Tech Wabag's earnings growth report.

- The valuation report we've compiled suggests that VA Tech Wabag's current price could be inflated.

Make It Happen

- Delve into our full catalog of 92 Fast Growing Indian Companies With High Insider Ownership here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Tega Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:TEGA

Tega Industries

Designs, manufactures, and installs process equipment and accessories for the mineral processing, mining, and material handling industries.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor