- India

- /

- Trade Distributors

- /

- NSEI:SIGIND

Does Signet Industries (NSE:SIGIND) Have A Healthy Balance Sheet?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Signet Industries Limited (NSE:SIGIND) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Signet Industries

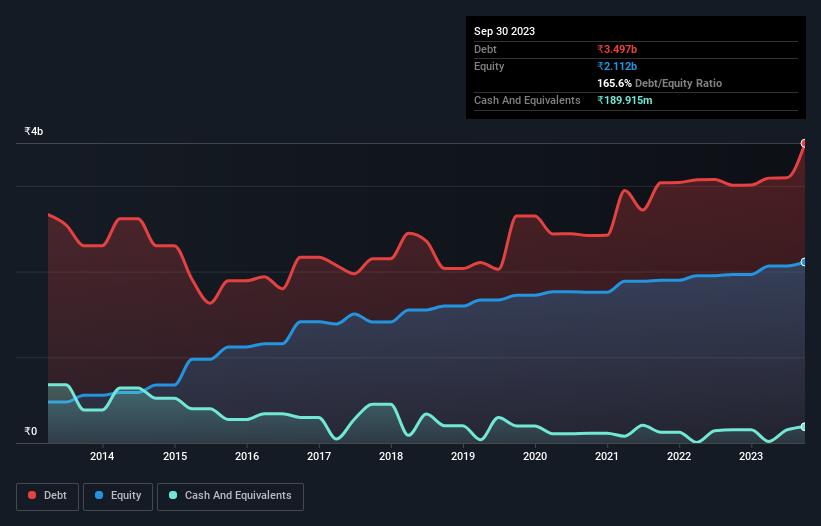

What Is Signet Industries's Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2023 Signet Industries had ₹3.50b of debt, an increase on ₹3.01b, over one year. However, it also had ₹189.9m in cash, and so its net debt is ₹3.31b.

A Look At Signet Industries' Liabilities

The latest balance sheet data shows that Signet Industries had liabilities of ₹4.65b due within a year, and liabilities of ₹733.0m falling due after that. On the other hand, it had cash of ₹189.9m and ₹3.33b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹1.86b.

This deficit is considerable relative to its market capitalization of ₹2.16b, so it does suggest shareholders should keep an eye on Signet Industries' use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Signet Industries's debt to EBITDA ratio (4.2) suggests that it uses some debt, its interest cover is very weak, at 1.7, suggesting high leverage. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. On the other hand, Signet Industries grew its EBIT by 27% in the last year. If it can maintain that kind of improvement, its debt load will begin to melt away like glaciers in a warming world. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Signet Industries will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. In the last three years, Signet Industries's free cash flow amounted to 35% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Signet Industries's struggle to cover its interest expense with its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. In particular, its EBIT growth rate was re-invigorating. When we consider all the factors discussed, it seems to us that Signet Industries is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 5 warning signs for Signet Industries (3 are concerning) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SIGIND

Signet Industries

Primarily engages in merchant trading of various polymer and plastic granules in India.

Good value slight.

Market Insights

Community Narratives