- India

- /

- Construction

- /

- NSEI:NBCC

It's Unlikely That Shareholders Will Increase NBCC (India) Limited's (NSE:NBCC) Compensation By Much This Year

The underwhelming performance at NBCC (India) Limited (NSE:NBCC) recently has probably not pleased shareholders. The next AGM coming up on 29 September 2022 will be a chance for shareholders to have their concerns addressed by the board, challenge management on company strategy and vote on resolutions such as executive remuneration, which may help change the company's future prospects. From our analysis below, we think CEO compensation looks appropriate for now.

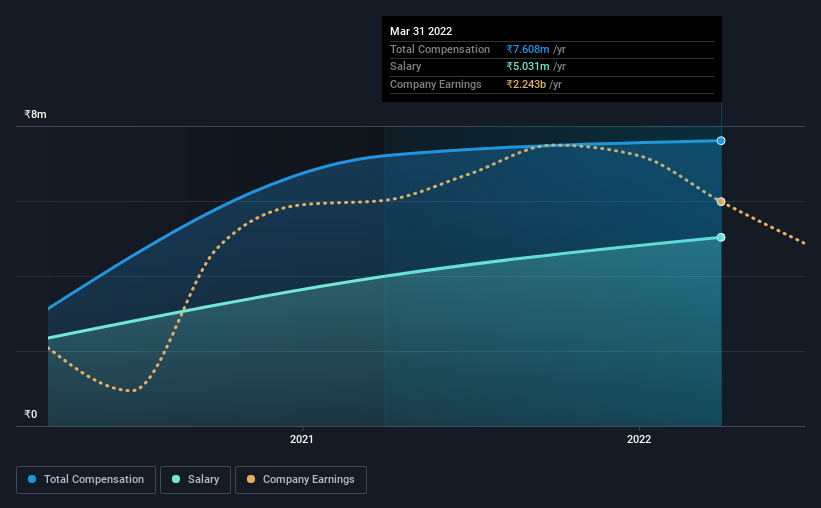

Check out our latest analysis for NBCC (India)

Comparing NBCC (India) Limited's CEO Compensation With The Industry

At the time of writing, our data shows that NBCC (India) Limited has a market capitalization of ₹61b, and reported total annual CEO compensation of ₹7.6m for the year to March 2022. That's just a smallish increase of 5.5% on last year. In particular, the salary of ₹5.03m, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the same industry with market capitalizations ranging between ₹32b and ₹128b had a median total CEO compensation of ₹48m. This suggests that Pawan Gupta is paid below the industry median.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | ₹5.0m | ₹4.0m | 66% |

| Other | ₹2.6m | ₹3.2m | 34% |

| Total Compensation | ₹7.6m | ₹7.2m | 100% |

Speaking on an industry level, nearly 97% of total compensation represents salary, while the remainder of 3% is other remuneration. It's interesting to note that NBCC (India) allocates a smaller portion of compensation to salary in comparison to the broader industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at NBCC (India) Limited's Growth Numbers

Over the last three years, NBCC (India) Limited has shrunk its earnings per share by 19% per year. It achieved revenue growth of 7.4% over the last year.

The decline in EPS is a bit concerning. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in EPS. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has NBCC (India) Limited Been A Good Investment?

With a three year total loss of 7.8% for the shareholders, NBCC (India) Limited would certainly have some dissatisfied shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, the board will get the chance to explain the steps it plans to take to improve business performance.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 3 warning signs for NBCC (India) that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you're looking to trade NBCC (India), open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NBCC (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NBCC

NBCC (India)

Engages in project management consultancy, engineering procurement and construction, and real estate development businesses in India and internationally.

Outstanding track record with excellent balance sheet.

Market Insights

Community Narratives