David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Hilton Metal Forging Limited (NSE:HILTON) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Hilton Metal Forging

How Much Debt Does Hilton Metal Forging Carry?

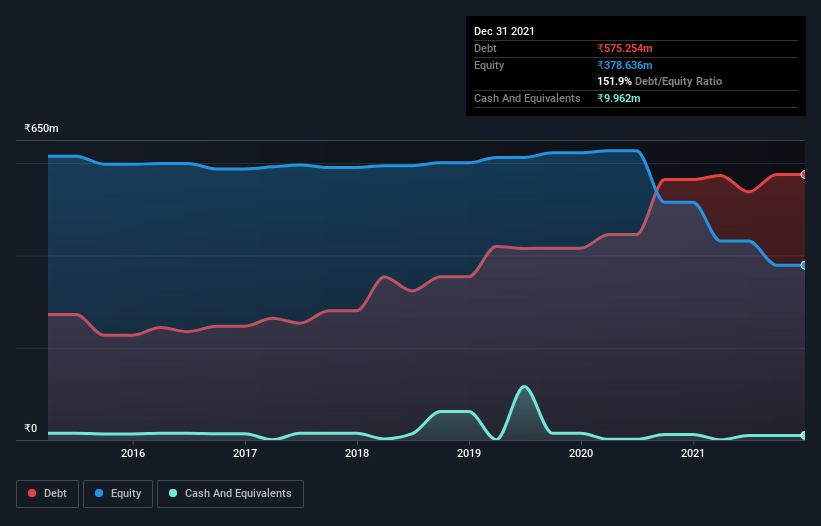

The chart below, which you can click on for greater detail, shows that Hilton Metal Forging had ₹575.3m in debt in September 2021; about the same as the year before. Net debt is about the same, since the it doesn't have much cash.

A Look At Hilton Metal Forging's Liabilities

Zooming in on the latest balance sheet data, we can see that Hilton Metal Forging had liabilities of ₹524.7m due within 12 months and liabilities of ₹166.2m due beyond that. Offsetting these obligations, it had cash of ₹9.96m as well as receivables valued at ₹91.1m due within 12 months. So it has liabilities totalling ₹589.8m more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the ₹310.5m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Hilton Metal Forging would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Hilton Metal Forging's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, Hilton Metal Forging reported revenue of ₹654m, which is a gain of 9.1%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, Hilton Metal Forging had an earnings before interest and tax (EBIT) loss over the last year. To be specific the EBIT loss came in at ₹5.3m. When we look at that alongside the significant liabilities, we're not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. For example, we would not want to see a repeat of last year's loss of ₹60m. And until that time we think this is a risky stock. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 4 warning signs for Hilton Metal Forging you should be aware of, and 2 of them can't be ignored.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Hilton Metal Forging might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HILTON

Hilton Metal Forging

Manufactures and sells iron and steel forgings for oil and gas, refinery, and pharmaceutical industries in India.

Slight with mediocre balance sheet.

Market Insights

Community Narratives