Advertisement

Read This Before You Buy Gujarat Apollo Industries Limited (NSE:GUJAPOLLO) Because Of Its P/E Ratio

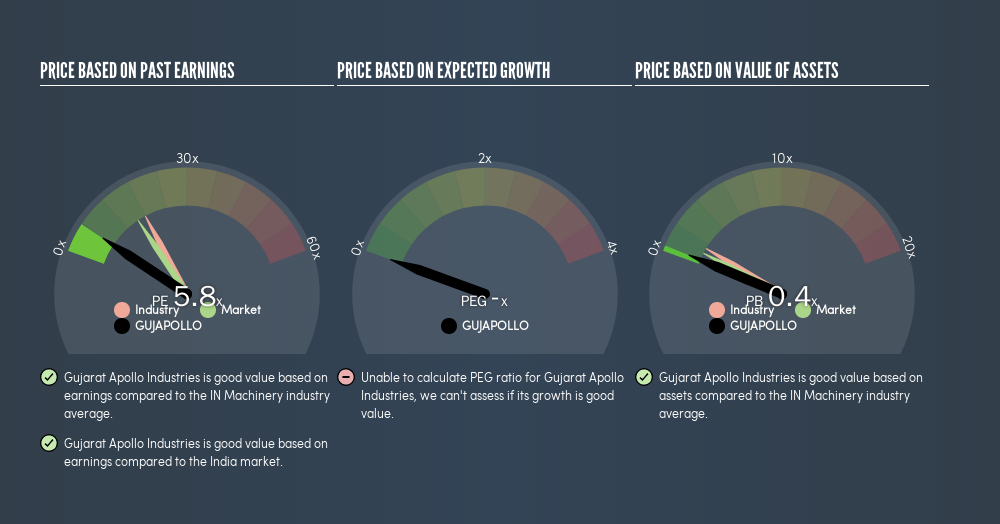

This article is written for those who want to get better at using price to earnings ratios (P/E ratios). We'll look at Gujarat Apollo Industries Limited's (NSE:GUJAPOLLO) P/E ratio and reflect on what it tells us about the company's share price. Gujarat Apollo Industries has a P/E ratio of 5.82, based on the last twelve months. In other words, at today's prices, investors are paying ₹5.82 for every ₹1 in prior year profit.

Check out our latest analysis for Gujarat Apollo Industries

How Do You Calculate A P/E Ratio?

The formula for P/E is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for Gujarat Apollo Industries:

P/E of 5.82 = ₹141 ÷ ₹24.23 (Based on the trailing twelve months to March 2018.)

Is A High P/E Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each ₹1 of company earnings. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. Earnings growth means that in the future the 'E' will be higher. That means even if the current P/E is high, it will reduce over time if the share price stays flat. Then, a lower P/E should attract more buyers, pushing the share price up.

Gujarat Apollo Industries saw earnings per share improve by -5.8% last year. And earnings per share have improved by 54% annually, over the last three years. But earnings per share are down 18% per year over the last five years.

How Does Gujarat Apollo Industries's P/E Ratio Compare To Its Peers?

The P/E ratio essentially measures market expectations of a company. The image below shows that Gujarat Apollo Industries has a lower P/E than the average (17.7) P/E for companies in the machinery industry.

Gujarat Apollo Industries's P/E tells us that market participants think it will not fare as well as its peers in the same industry. While current expectations are low, the stock could be undervalued if the situation is better than the market assumes. If you consider the stock interesting, further research is recommended. For example, I often monitor director buying and selling.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

Don't forget that the P/E ratio considers market capitalization. Thus, the metric does not reflect cash or debt held by the company. Theoretically, a business can improve its earnings (and produce a lower P/E in the future), by taking on debt (or spending its remaining cash).

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

Is Debt Impacting Gujarat Apollo Industries's P/E?

Since Gujarat Apollo Industries holds net cash of ₹252m, it can spend on growth, justifying a higher P/E ratio than otherwise.

The Verdict On Gujarat Apollo Industries's P/E Ratio

Gujarat Apollo Industries's P/E is 5.8 which is below average (15.5) in the IN market. EPS was up modestly better over the last twelve months. And the healthy balance sheet means the company can sustain growth while the P/E suggests shareholders don't think it will.

Investors have an opportunity when market expectations about a stock are wrong. If the reality for a company is not as bad as the P/E ratio indicates, then the share price should increase as the market realizes this. Although we don't have analyst forecasts, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

You might be able to find a better buy than Gujarat Apollo Industries. If you want a selection of possible winners, check out this freelist of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:GUJAPOLLO

Gujarat Apollo Industries

Manufactures and sells crushing and screening equipment for construction, mining, and general infrastructure development in India and internationally.

Moderate with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor