Advertisement

- India

- /

- Construction

- /

- NSEI:GENCON

Why Generic Engineering Construction and Projects' (NSE:GENCON) Shaky Earnings Are Just The Beginning Of Its Problems

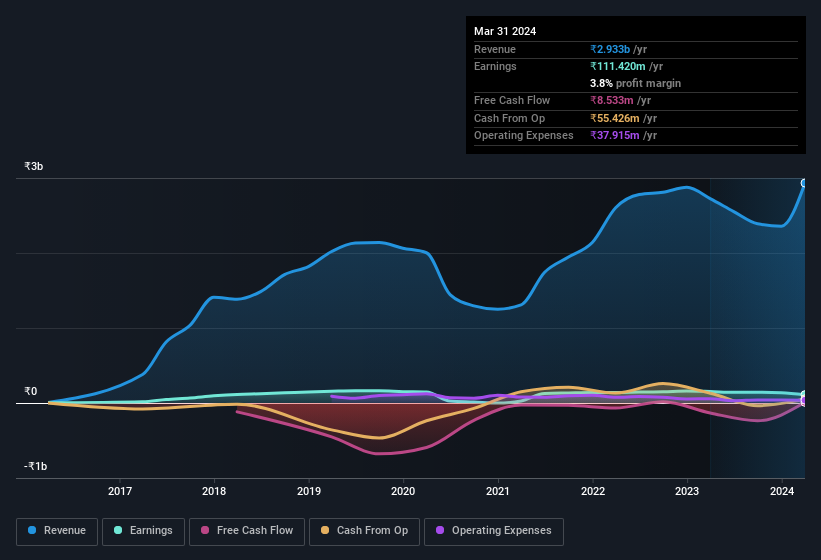

The subdued market reaction suggests that Generic Engineering Construction and Projects Limited's (NSE:GENCON) recent earnings didn't contain any surprises. Our analysis suggests that along with soft profit numbers, investors should be aware of some other underlying weaknesses in the numbers.

See our latest analysis for Generic Engineering Construction and Projects

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. As it happens, Generic Engineering Construction and Projects issued 9.5% more new shares over the last year. That means its earnings are split among a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of Generic Engineering Construction and Projects' EPS by clicking here.

A Look At The Impact Of Generic Engineering Construction and Projects' Dilution On Its Earnings Per Share (EPS)

As you can see above, Generic Engineering Construction and Projects has been growing its net income over the last few years, with an annualized gain of 300% over three years. But EPS was only up 221% per year, in the exact same period. Net income was down 27% over the last twelve months. Unfortunately for shareholders, though, the earnings per share result was even worse, declining 27%. And so, you can see quite clearly that dilution is influencing shareholder earnings.

In the long term, if Generic Engineering Construction and Projects' earnings per share can increase, then the share price should too. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Generic Engineering Construction and Projects.

Our Take On Generic Engineering Construction and Projects' Profit Performance

Over the last year Generic Engineering Construction and Projects issued new shares and so, there's a noteworthy divergence between EPS and net income growth. Because of this, we think that it may be that Generic Engineering Construction and Projects' statutory profits are better than its underlying earnings power. But on the bright side, its earnings per share have grown at an extremely impressive rate over the last three years. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you'd like to know more about Generic Engineering Construction and Projects as a business, it's important to be aware of any risks it's facing. You'd be interested to know, that we found 3 warning signs for Generic Engineering Construction and Projects and you'll want to know about these.

This note has only looked at a single factor that sheds light on the nature of Generic Engineering Construction and Projects' profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:GENCON

Generic Engineering Construction and Projects

Engages in the construction of commercial, residential, industrial, health and leisure, and institutional buildings in India.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

159 followersusers have followed this narrative

0 commentsusers have commented on this narrative

27 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

JR

JRY on Bloom Energy ·

The Bloom Story is early days

Fair Value:US$386.143.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CH

ChuckN on NextEra Energy ·

Investor Thesis: Why the NextEra Energy / Dominion Energy Merger Could Be a Major AI Power Infrastructure Event

Fair Value:US$93.719.7% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.1% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

281 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

143 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

166 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0