Advertisement

Do Beardsell's (NSE:BEARDSELL) Earnings Warrant Your Attention?

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Beardsell (NSE:BEARDSELL). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

View our latest analysis for Beardsell

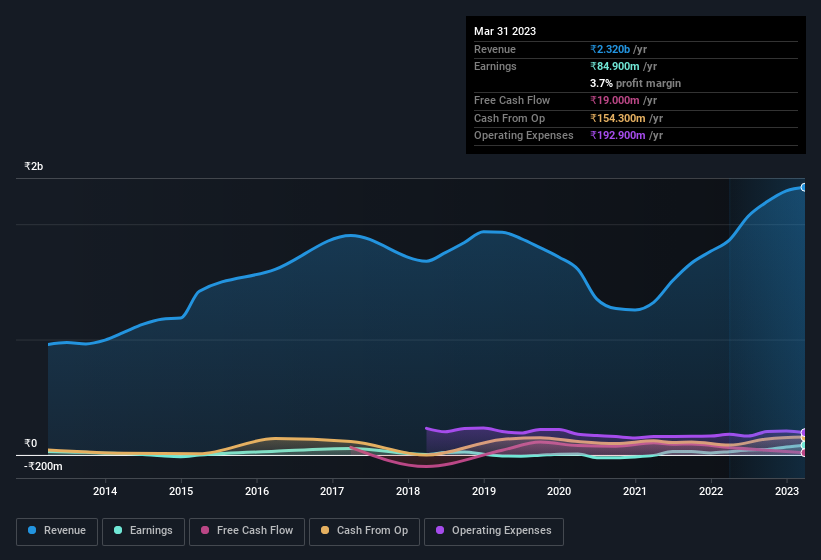

Beardsell's Improving Profits

Over the last three years, Beardsell has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. So it would be better to isolate the growth rate over the last year for our analysis. Impressively, Beardsell's EPS catapulted from ₹0.94 to ₹2.15, over the last year. Year on year growth of 129% is certainly a sight to behold.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. EBIT margins for Beardsell remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 25% to ₹2.3b. That's progress.

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

Beardsell isn't a huge company, given its market capitalisation of ₹1.2b. That makes it extra important to check on its balance sheet strength.

Are Beardsell Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Belief in the company remains high for insiders as there hasn't been a single share sold by the management or company board members. But the real excitement comes from the ₹8.9m that Whole-time Director Jayasree Anumolu spent buying shares (at an average price of about ₹23.85). Purchases like this clue us in to the to the faith management has in the business' future.

And the insider buying isn't the only sign of alignment between shareholders and the board, since Beardsell insiders own more than a third of the company. In fact, they own 47% of the shares, making insiders a very influential shareholder group. Those who are comforted by solid insider ownership like this should be happy, as it implies that those running the business are genuinely motivated to create shareholder value. Valued at only ₹1.2b Beardsell is really small for a listed company. So this large proportion of shares owned by insiders only amounts to ₹549m. This isn't an overly large holding but it should still keep the insiders motivated to deliver the best outcomes for shareholders.

Is Beardsell Worth Keeping An Eye On?

Beardsell's earnings have taken off in quite an impressive fashion. The icing on the cake is that insiders own a large chunk of the company and one has even been buying more shares. These factors seem to indicate the company's potential and that it has reached an inflection point. We'd suggest Beardsell belongs near the top of your watchlist. You still need to take note of risks, for example - Beardsell has 4 warning signs (and 2 which are a bit concerning) we think you should know about.

Keen growth investors love to see insider buying. Thankfully, Beardsell isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Beardsell might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BEARDSELL

Beardsell

Manufactures and supplies expanded polystyrene (EPS) products and prefabricated buildings for various industrial applications in India and internationally.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor