Advertisement

Balu Forge Industries Limited (NSE:BALUFORGE) May Have Run Too Fast Too Soon With Recent 27% Price Plummet

The Balu Forge Industries Limited (NSE:BALUFORGE) share price has fared very poorly over the last month, falling by a substantial 27%. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

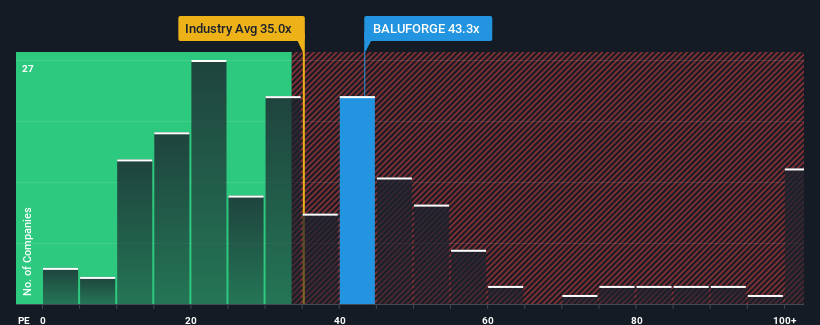

In spite of the heavy fall in price, given around half the companies in India have price-to-earnings ratios (or "P/E's") below 29x, you may still consider Balu Forge Industries as a stock to potentially avoid with its 43.3x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Recent times have been advantageous for Balu Forge Industries as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Balu Forge Industries

Does Growth Match The High P/E?

There's an inherent assumption that a company should outperform the market for P/E ratios like Balu Forge Industries' to be considered reasonable.

Retrospectively, the last year delivered an exceptional 71% gain to the company's bottom line. Pleasingly, EPS has also lifted 375% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 13% as estimated by the only analyst watching the company. Meanwhile, the rest of the market is forecast to expand by 26%, which is noticeably more attractive.

With this information, we find it concerning that Balu Forge Industries is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Bottom Line On Balu Forge Industries' P/E

Despite the recent share price weakness, Balu Forge Industries' P/E remains higher than most other companies. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Balu Forge Industries' analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Plus, you should also learn about this 1 warning sign we've spotted with Balu Forge Industries.

Of course, you might also be able to find a better stock than Balu Forge Industries. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Balu Forge Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BALUFORGE

Balu Forge Industries

Manufactures and sells crankshafts in India and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.2% undervalued

TO

Community Contributor