Should You Consider Astral Poly Technik Limited (NSE:ASTRAL)?

Astral Poly Technik Limited (NSE:ASTRAL) is a company with exceptional fundamental characteristics. Upon building up an investment case for a stock, we should look at various aspects. In the case of ASTRAL, it is a financially-healthy company with a great history and an optimistic growth outlook. In the following section, I expand a bit more on these key aspects. For those interested in digger a bit deeper into my commentary, read the full report on Astral Poly Technik here.

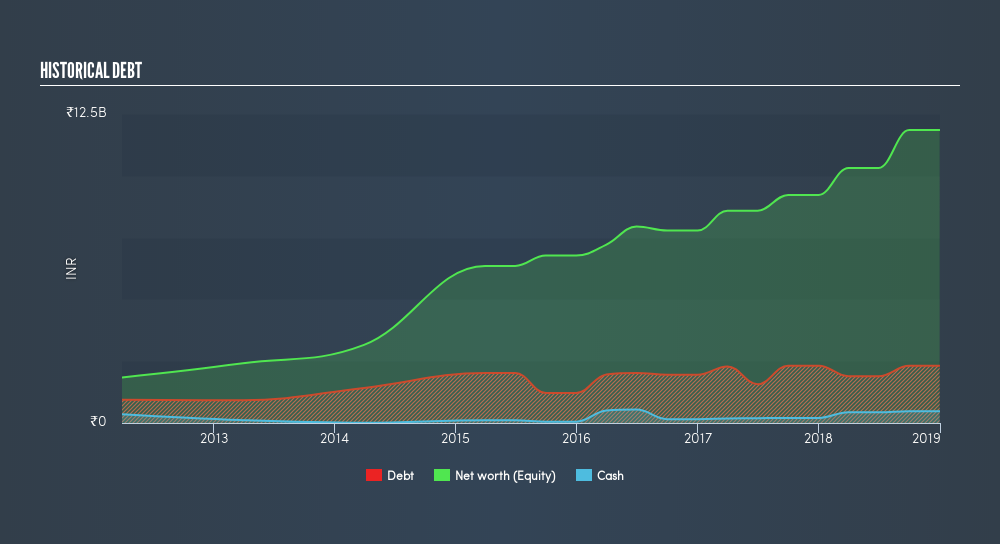

Flawless balance sheet with high growth potential

One reason why investors are attracted to ASTRAL is its earnings growth potential in the near future of 25% which is expected to flow into an impressive return on equity of 21% over the next couple of years. Over the past few years, ASTRAL has demonstrated a proven ability to generate robust returns of 11% Not surprisingly, ASTRAL outperformed its industry which returned 6.4%, giving us more conviction of the company's capacity to drive bottom-line growth going forward.

ASTRAL is financially robust, with ample cash on hand and short-term investments to meet upcoming liabilities. This indicates that ASTRAL has sufficient cash flows and proper cash management in place, which is an important determinant of the company’s health. ASTRAL's has produced operating cash levels of 1.22x total debt over the past year, which implies that ASTRAL's management has put its borrowings into good use by generating enough cash to cover a sufficient portion of borrowings.

Next Steps:

For Astral Poly Technik, there are three key aspects you should look at:

- Valuation: What is ASTRAL worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether ASTRAL is currently mispriced by the market.

- Dividend Income vs Capital Gains: Does ASTRAL return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from ASTRAL as an investment.

- Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of ASTRAL? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NSEI:ASTRAL

Astral

Engages in the manufacture and marketing of pipes, water tanks, and adhesives and sealants in India and internationally.

Flawless balance sheet with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Community Narratives