Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies The Anup Engineering Limited (NSE:ANUP) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Anup Engineering

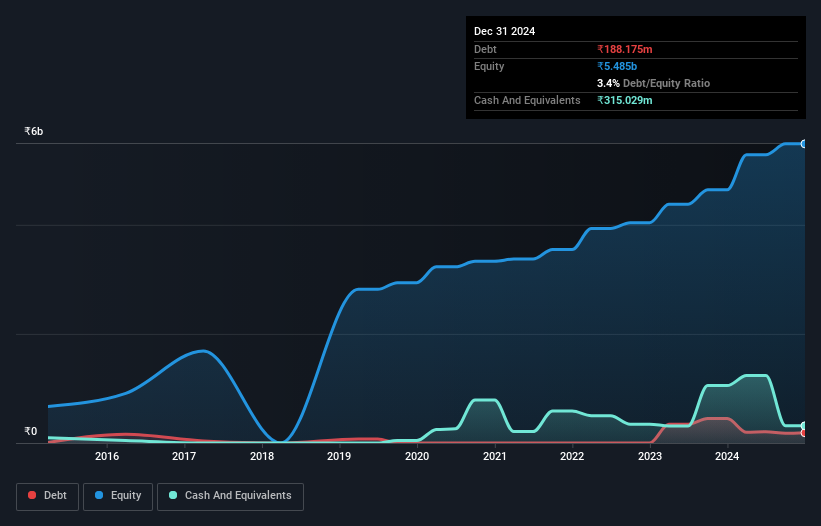

What Is Anup Engineering's Debt?

The image below, which you can click on for greater detail, shows that Anup Engineering had debt of ₹188.2m at the end of September 2024, a reduction from ₹448.3m over a year. However, its balance sheet shows it holds ₹315.0m in cash, so it actually has ₹126.9m net cash.

A Look At Anup Engineering's Liabilities

We can see from the most recent balance sheet that Anup Engineering had liabilities of ₹2.95b falling due within a year, and liabilities of ₹282.6m due beyond that. Offsetting these obligations, it had cash of ₹315.0m as well as receivables valued at ₹2.29b due within 12 months. So it has liabilities totalling ₹625.7m more than its cash and near-term receivables, combined.

Having regard to Anup Engineering's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the ₹60.3b company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, Anup Engineering also has more cash than debt, so we're pretty confident it can manage its debt safely.

Another good sign is that Anup Engineering has been able to increase its EBIT by 25% in twelve months, making it easier to pay down debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Anup Engineering's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Anup Engineering has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Anup Engineering's free cash flow amounted to 22% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing Up

We could understand if investors are concerned about Anup Engineering's liabilities, but we can be reassured by the fact it has has net cash of ₹126.9m. And it impressed us with its EBIT growth of 25% over the last year. So we don't think Anup Engineering's use of debt is risky. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Anup Engineering insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ANUP

Anup Engineering

Manufactures and fabricates process equipment for oil and gas, petrochemicals, LNG, fertilizers, chemicals, hydrogen, pharmaceuticals, power, water, paper and pulp, and aerospace industries in India.

Exceptional growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor