Stock Analysis

Be Wary Of Tata Motors (NSE:TATAMTRDVR) And Its Returns On Capital

To avoid investing in a business that's in decline, there's a few financial metrics that can provide early indications of aging. When we see a declining return on capital employed (ROCE) in conjunction with a declining base of capital employed, that's often how a mature business shows signs of aging. Ultimately this means that the company is earning less per dollar invested and on top of that, it's shrinking its base of capital employed. Having said that, after a brief look, Tata Motors (NSE:TATAMTRDVR) we aren't filled with optimism, but let's investigate further.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Tata Motors, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.0038 = ₹6.9b ÷ (₹3.3t - ₹1.5t) (Based on the trailing twelve months to June 2022).

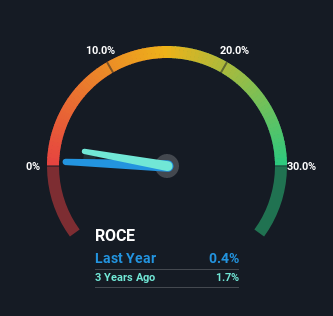

Thus, Tata Motors has an ROCE of 0.4%. Ultimately, that's a low return and it under-performs the Auto industry average of 19%.

See our latest analysis for Tata Motors

In the above chart we have measured Tata Motors' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Tata Motors here for free.

The Trend Of ROCE

In terms of Tata Motors' historical ROCE movements, the trend doesn't inspire confidence. About five years ago, returns on capital were 3.8%, however they're now substantially lower than that as we saw above. And on the capital employed front, the business is utilizing roughly the same amount of capital as it was back then. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Tata Motors to turn into a multi-bagger.

On a side note, Tata Motors' current liabilities are still rather high at 46% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Key Takeaway

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. And long term shareholders have watched their investments stay flat over the last five years. Unless there is a shift to a more positive trajectory in these metrics, we would look elsewhere.

Tata Motors could be trading at an attractive price in other respects, so you might find our free intrinsic value estimation on our platform quite valuable.

While Tata Motors isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're helping make it simple.

Find out whether Tata Motors is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TATAMTRDVR

Tata Motors

Designs, develops, manufactures, and sells various automotive vehicles.

Solid track record with adequate balance sheet and pays a dividend.