Advertisement

- India

- /

- Auto Components

- /

- NSEI:SUNDRMFAST

Sundram Fasteners Limited Just Recorded A 39% EPS Beat: Here's What Analysts Are Forecasting Next

As you might know, Sundram Fasteners Limited (NSE:SUNDRMFAST) just kicked off its latest quarterly results with some very strong numbers. It was a solid earnings report, with revenues and statutory earnings per share (EPS) both coming in strong. Revenues were 12% higher than the analysts had forecast, at ₹11b, while EPS were ₹5.69 beating analyst models by 39%. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for Sundram Fasteners

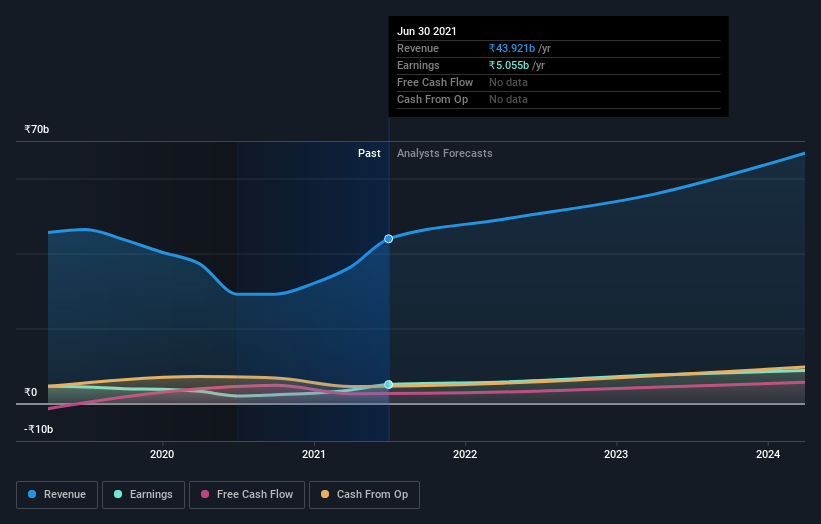

Taking into account the latest results, the current consensus from Sundram Fasteners' three analysts is for revenues of ₹49.1b in 2022, which would reflect a decent 12% increase on its sales over the past 12 months. Per-share earnings are expected to step up 18% to ₹28.40. In the lead-up to this report, the analysts had been modelling revenues of ₹46.1b and earnings per share (EPS) of ₹25.95 in 2022. It looks like there's been a modest increase in sentiment following the latest results, withthe analysts becoming a bit more optimistic in their predictions for both revenues and earnings.

It will come as no surprise to learn that the analysts have increased their price target for Sundram Fasteners 7.4% to ₹874on the back of these upgrades. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Sundram Fasteners analyst has a price target of ₹900 per share, while the most pessimistic values it at ₹799. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Sundram Fasteners is an easy business to forecast or the the analysts are all using similar assumptions.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's pretty clear that there is an expectation that Sundram Fasteners' revenue growth will slow down substantially, with revenues to the end of 2022 expected to display 16% growth on an annualised basis. This is compared to a historical growth rate of 51% over the past year. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 13% annually. So it's pretty clear that, while Sundram Fasteners' revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Sundram Fasteners following these results. There was also an upgrade to revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for Sundram Fasteners going out to 2024, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 1 warning sign for Sundram Fasteners you should know about.

If you’re looking to trade Sundram Fasteners, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:SUNDRMFAST

Sundram Fasteners

Manufactures and sells precision components for the automotive, infrastructure, wind energy, aerospace, defense, farm equipment, industrial, aviation, and other sectors in India, China, the United States, the United Kingdom, and internationally.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor