Advertisement

- India

- /

- Auto Components

- /

- NSEI:SUNDRMBRAK

Here's Why Sundaram Brake Linings (NSE:SUNDRMBRAK) Can Manage Its Debt Responsibly

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Sundaram Brake Linings Limited (NSE:SUNDRMBRAK) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Sundaram Brake Linings

What Is Sundaram Brake Linings's Net Debt?

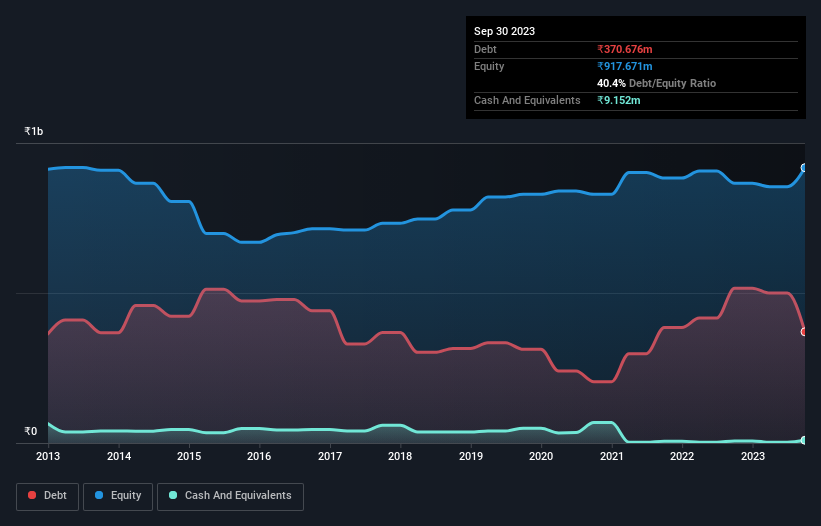

As you can see below, Sundaram Brake Linings had ₹370.7m of debt at September 2023, down from ₹516.0m a year prior. However, it also had ₹9.15m in cash, and so its net debt is ₹361.5m.

A Look At Sundaram Brake Linings' Liabilities

According to the last reported balance sheet, Sundaram Brake Linings had liabilities of ₹848.5m due within 12 months, and liabilities of ₹152.7m due beyond 12 months. Offsetting this, it had ₹9.15m in cash and ₹658.3m in receivables that were due within 12 months. So its liabilities total ₹333.8m more than the combination of its cash and short-term receivables.

Of course, Sundaram Brake Linings has a market capitalization of ₹2.63b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Sundaram Brake Linings has a quite reasonable net debt to EBITDA multiple of 2.4, its interest cover seems weak, at 2.3. This does have us wondering if the company pays high interest because it is considered risky. In any case, it's safe to say the company has meaningful debt. Notably, Sundaram Brake Linings made a loss at the EBIT level, last year, but improved that to positive EBIT of ₹89m in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But it is Sundaram Brake Linings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, Sundaram Brake Linings actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

When it comes to the balance sheet, the standout positive for Sundaram Brake Linings was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren't so heartening. In particular, interest cover gives us cold feet. When we consider all the elements mentioned above, it seems to us that Sundaram Brake Linings is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 1 warning sign for Sundaram Brake Linings that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SUNDRMBRAK

Sundaram Brake Linings

Manufactures and sells asbestos free friction materials in India and internationally.

Slight risk with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.7% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|18.7% undervalued

GM

Community Contributor