Advertisement

- India

- /

- Auto Components

- /

- NSEI:SJS

Broker Revenue Forecasts For S.J.S. Enterprises Limited (NSE:SJS) Are Surging Higher

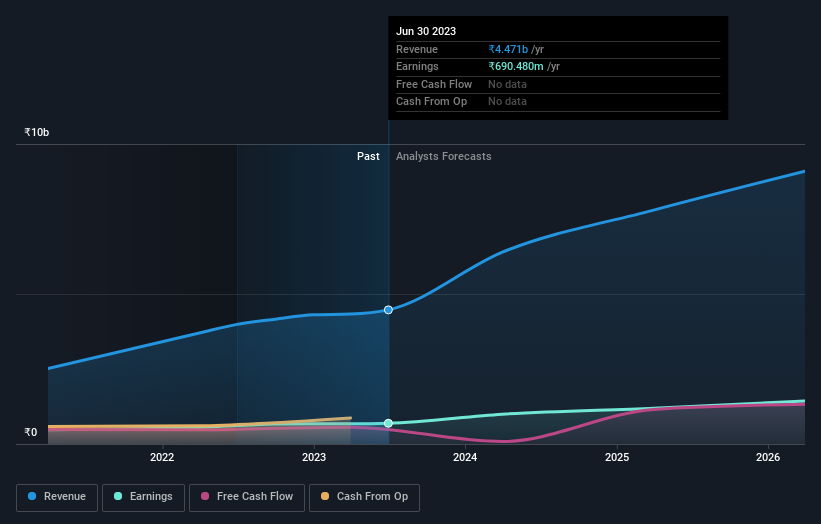

S.J.S. Enterprises Limited (NSE:SJS) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects. The market seems to be pricing in some improvement in the business too, with the stock up 9.8% over the past week, closing at ₹669. Could this big upgrade push the stock even higher?

After the upgrade, the three analysts covering S.J.S. Enterprises are now predicting revenues of ₹6.4b in 2024. If met, this would reflect a major 43% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to shoot up 44% to ₹32.03. Before this latest update, the analysts had been forecasting revenues of ₹5.4b and earnings per share (EPS) of ₹29.45 in 2024. The most recent forecasts are noticeably more optimistic, with a substantial gain in revenue estimates and a lift to earnings per share as well.

See our latest analysis for S.J.S. Enterprises

With these upgrades, we're not surprised to see that the analysts have lifted their price target 15% to ₹729 per share. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values S.J.S. Enterprises at ₹850 per share, while the most bearish prices it at ₹566. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that S.J.S. Enterprises' rate of growth is expected to accelerate meaningfully, with the forecast 61% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 12% over the past year. Compare this with other companies in the same industry, which are forecast to grow their revenue 10% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect S.J.S. Enterprises to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. They also upgraded their revenue estimates for this year, and sales are expected to grow faster than the wider market. There was also a nice increase in the price target, with analysts apparently feeling that the intrinsic value of the business is improving. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at S.J.S. Enterprises.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have estimates - from multiple S.J.S. Enterprises analysts - going out to 2026, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SJS

S.J.S. Enterprises

Designs, develops, manufactures, sells, and exports decorative aesthetics primarily to automotive and consumer appliance industries in India and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor