Advertisement

- India

- /

- Auto Components

- /

- NSEI:RBL

The Returns On Capital At Rane Brake Lining (NSE:RBL) Don't Inspire Confidence

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Although, when we looked at Rane Brake Lining (NSE:RBL), it didn't seem to tick all of these boxes.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Rane Brake Lining, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.14 = ₹314m ÷ (₹3.4b - ₹1.1b) (Based on the trailing twelve months to December 2020).

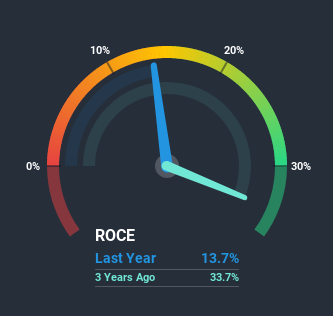

Thus, Rane Brake Lining has an ROCE of 14%. On its own, that's a standard return, however it's much better than the 8.6% generated by the Auto Components industry.

See our latest analysis for Rane Brake Lining

Historical performance is a great place to start when researching a stock so above you can see the gauge for Rane Brake Lining's ROCE against it's prior returns. If you're interested in investigating Rane Brake Lining's past further, check out this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

On the surface, the trend of ROCE at Rane Brake Lining doesn't inspire confidence. Over the last five years, returns on capital have decreased to 14% from 23% five years ago. Given the business is employing more capital while revenue has slipped, this is a bit concerning. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

Our Take On Rane Brake Lining's ROCE

From the above analysis, we find it rather worrisome that returns on capital and sales for Rane Brake Lining have fallen, meanwhile the business is employing more capital than it was five years ago. Since the stock has skyrocketed 139% over the last five years, it looks like investors have high expectations of the stock. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

One more thing: We've identified 3 warning signs with Rane Brake Lining (at least 1 which shouldn't be ignored) , and understanding them would certainly be useful.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you decide to trade Rane Brake Lining, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:RBL

Rane Brake Lining

Manufactures and markets auto components to original equipment manufacturers and aftermarket customers in India and internationally.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor